We catch up with the exciting developments from LafargeHolcim’s Mannersdorf plant in Lower Austria, which include plans for full-scale CO2 capture and utilisation.

Plant profile: Lafarge Zement Mannersdorf

| Site established: 1894 | 1894 |

| Kilns: | One - PASEC System - Commissioned 1984 |

| Design capacity: | 2730t/day (0.9Mt/yr) clinker |

| 1.4Mt/yr cement | |

| Capacity today: | 2500t/day (0.8Mt/yr) clinker |

| 1.2Mt/yr cement | |

| Raw mill: | 200t/hr roller press - KHD tandem mill |

| Finish ball mills: | 60t/hr - FLSmidth |

| 115t/hr - Krupp Polysius |

Global Cement (GC): Please could you outline the history of the Mannersdorf cement plant?

Christopher Ehrenberg (CE): The site of the Mannersdorf plant was first established as an industrial facility in 1894. The first rotary kiln for cement came online in 1904, with a series of wet kilns subsequently added. In 1968 the plant received its first dry line, kiln No. 8, a KHD four-stage preheater line with a capacity of around 0.8Mt/yr of cement. In 1984 we moved to a pre-calciner system. In 2017 the relatively small separate line calciner was replaced by a large inline calciner to boost alternative fuel usage.

Plant and process

GC: What is the production process used today?

CE: The current preheater from 1984 is a Parallel Air Serial Combustion (PASEC) system. It is rare because only a few were ever built by a joint venture between Voest Alpine Austria and the East German company Sket ZAB Dessau. The preheater has five stages with two strings. The gas flow is parallel but the material jumps from string to string - leading to better thermal efficiency, on the other hand causing high pressure loss. It was built in that way to bring down the specific heat consumption. The original design had an exhaust temperature of less than 300°C. With the changes that we have made to the line since then, including the introduction of alternative fuels, the exhaust temperature is now slightly higher, around 330°C. This is also needed to cope with increasing raw material moisture.

The kiln’s rated capacity is 2730t/day, which is around 0.9Mt/yr of clinker or 1.4Mt/yr of cement. To boost the use of alternative fuels and to improve the thermal efficiency a large inline calciner (ILC) with separate tower in front of the existing tower was erected 2016 - 2017. The ILC has a gas residence time of more than 7s. Our alternative fuel rate was boosted by this to above 90% on stable days, with 100% refuse-derived fuel (RDF) at the calciner.

The raw mill shop, partly still from the older KHD line from 1968, is the remaining bottleneck, especially due to increasing limestone moisture. This led to the decision to install a new vertical raw mill from Loesche, which will be commissioned in 2022.

GC: Where does the plant source its raw material?

CE: We have two quarries, one of which contains >95% CaCO3 limestone and one of which contains clay. Between the limestone quarry and the plant is the town of Mannersdorf. The material is transported via belt through the town over a distance of 1.5km. The clay is from a clay pit located adjacent to the plant.

In 2005 we started to use our first alternative raw material, replacing the clay partly with recycled clay bricks. This is one of our most important contributions to recycling. Around 0.18Mt/yr of brick waste from end-of-life buildings in the Vienna area has now replaced almost two thirds of our natural clay demand. We mix natural clay in layers with the bricks and then ‘excavate’ the mixture, which acts as a ‘raw’ material.

Continuing with the flow, the material from the quarry, clay bricks and other materials are stored in the raw mix hall, which has a capacity of 40,000t. The current KHD raw mill system comprises a hammer pre-crusher with a roller press. The plant has two cement ball mills. One was produced by FLSmidth and it operates with a KHD roller press. The other is from Krupp Polysius with a third-generation separator. Our 10 cement silos have a total storage of 54,000t.

GC: What types of cement are produced?

CE: We produce nine types of cement at the Mannersdorf plant. The plant has a high share of CEM II cements and an average clinker factor of 67%. It makes around 15 - 20% CEM I, half of which is C3A-free, and 70% CEM II. The remaining 10% of our output is a concrete additive called Fluamix C.

In addition to the normal types of cement, we make a special C3A-free clinker called Contragress. This is used for applications that require sulphate-resistance and it is widely used in the Viennese market. The entire Vienna Metro system is made from Contragress-based concrete. Fluamix C has no clinker in it at all. It is used as an additive in concrete mixtures that may contain other types of cement.

GC: What fuels does the plant use?

CE: The plant began using alternative fuels in 1996, with animal meal and liquid fuels. Over time the plant has increased rapidly from 10% in 1998 to 27% in 2000, 35% in 2002, 40% in 2004, 45% in 2010, 60% in 2012 and 85% in 2019. In 2020 this dropped dramatically due to a fire in the alternative fuel hall in June. Our current substitution rate is affected, but we will rise above 90% again later this year thanks to the installation of a new alternative fuels hall and feeding and dosing equipment.

A step change was the start-up of the inline calciner in 2017. This allowed us to saturate the calciner with coarse RDF without need of a control fuel. All RDF is dosed from the alternative fuel hall and docking stations, fed via tube conveyor and using a screw as an air lock into the calciner. On the main burner we use high grade RDF via satellite burner, solvents, waste oil and a small amount of petcoke.

GC: What fuels were used in 2020?

CE: Due to the fire 2020 was not a representative year. However, in 2019 we used on average 85% alternative fuels, with close to 100% on the best days. The calciner can now be saturated with coarse RDF and we only switch to petcoke in case of dosing disturbances. The main burner, representing 40% of the total, has a mix of high grade RDF, liquids, some waste tyres and a small amount of petcoke.

GC: How did the plant handle the change to a low level of alternative fuels?

CE: It was a strange situation, because no plant ever plans to drop from nearly 100% alternative fuels to a low level. The operators had to relearn how to use 90% petcoke and it was a steep learning curve. It felt like we were going back 20 years in time. We now have an intermediate solution and hope to commission the new Beumer / Schenck equipment incrementally over the summer of 2021. This shows the resilience of our excellent staff.

GC: What emissions abatement systems are installed at the plant?

CE: For NOx control we had historically employed a selective non-catalytic reduction (SNCR) system. However, since 2012 and the installation of our semi-dust selective catalytic reduction (SCR) system from Scheuch, this has been employed only as a back up. The semi-dust SCR was the first SCR in Austria and among the first in the world. An ESP is used to dedust the preheater exit gas before two catalyst layers. The SCR, after some optimisation, enables us to achieve 200mg/Nm3 in stable operation. An annual average of almost 200mg/Nm³ could also be achieved, thanks to the lower raw NOx when running the inline calciner with RDF.

With respect to our dust emissions, we have a legal limit of 20mg/Nm3. However, we have self-limited to 8mg/Nm3. We communicate our dust emissions monthly along with other parameters like vibration levels from quarry blasts. We want to be really open and transparent because we have found that this creates trust between the plant and its stakeholders.

SO2 emissions fell sharply in 2005 with the introduction of waste clay bricks to the process. We are at a very low level of SO2 emissions. There is also continuous measurement of mercury, which began in 2011. When we installed the device, we began to see the spikes that happen when, for example, the raw mill stops. We use active carbon injection to counter these. We have a limit for total organic carbon (TOC), which we have always been able to adhere to comfortably. The SCR and large calciner have helped in this regard.

GC: What projects are currently taking place?

CE: There are three large projects currently taking place at the plant. Firstly, the new vertical raw mill will replace the 53 year old raw mill shop from 1968. The VRM, a Loesche LM 45.4, will be erected parallel to the existing raw mill. This will represent a ‘game-changer’ for the plant and is very important for our continued development. The existing material dosing bins will be reused as well as raw meal transport and storage silos. The new mill is due to begin operations in February 2022, when the new raw mill will be connected to the material and gas stream during winter kiln stoppage. The existing kiln bag filter will also be re-used.

The new vertical raw mill will have a capacity of 275t/hr, removing the main bottleneck of today’s kiln line. It will reduce significantly the electrical power consumption. In addition to raw mix, the vertical roller mill will be used in campaigns to grind limestone for cement. Separate grinding of limestone and mixing this into our base product will allow us to optimise our product portfolio even further and will reduce electrical power used for cement grinding too.

The second major project is the installation of a new RDF flash dryer, which is presently being erected. It is scheduled for commissioning in the summer of 2021 and is being supplied by A TEC. It will allow up to 6t/hr of main burner RDF to be dried before firing in a satellite burner. The reduction of moisture will improve the main burner flame, which will allow the plant to increase its RDF use further. The hot gas source for the flash dryer will be bypass exit gas from after the bag filter, or cooler exit gas after the electrostatic precipitator. The gas from after the flash dryer cyclone and filter will be re-introduced to the cooler fan inlet. This will destroy odors from RDF drying.

The third project is the reconstruction of the RDF hall, dosing and transport after the fire in June 2020, and is fully underway. Beumer and Schenck are installing equipment for extraction, dosing and pipe conveyors. Calciner RDF transport will be provided by a 195m-long Beumer Pipe Conveyor. RDF will be sourced from two identical 50m³ dosing bins on the calciner pipe, in addition to one dosing from a docking station. The main burner RDF will be stored in a separate box in the hall and fed by the crane to a 50m³ bin. It will be dosed to the main burner via a second Beumer Pipe Conveyor. Hall, dosing and conveyors will be equipped with a state of the art fire detection and extinguishing system. Start up will be in steps - full operation with automatic crane and all dosing lines will be attained in the autumn of 2021.

C2PAT Project

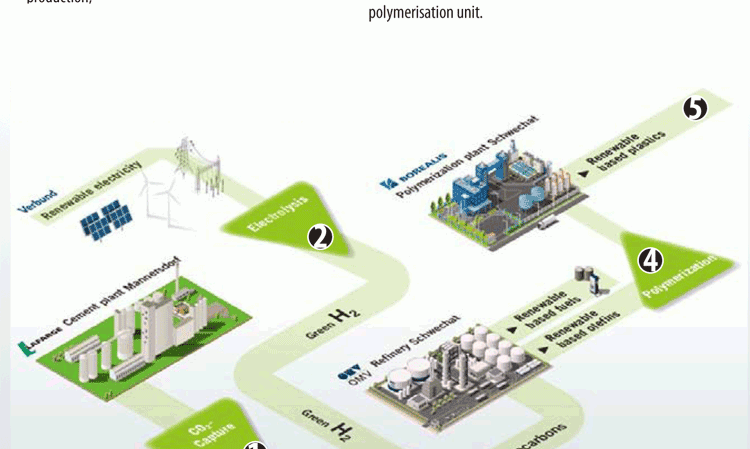

Joseph Kitzweger, Director of Sustainable Development, LafargeHolcim Austria (JK): The Mannersdorf plant is involved in a huge CO2 capture and utilisation (CCU) project known as Carbon2ProductAustria (C2PAT). In this project, we aim to demonstrate a novel, first-of-its-kind cross-sectoral circular carbon value chain on an industrial scale. CO2 from cement production will be captured and combined with renewably-generated hydrogen to produce a feedstock for chemical processes. This will be converted into renewable plastics and fuels.

With our partners OMV (refinery), Verbund (renewable electricity provider) and Borealis (chemical and plastics producer), we will integrate and operate different technologies that will be combined into one novel holistic value chain (Figure 1).

LafargeHolcim was the leading force in the formation of the consortium. We contacted the other partners, each of which was keen to join us due to different motivations. Plastics and refineries will have to adapt to a fossil fuel-free world in the coming decades and renewable power will come in to fill the gap in power generation that opens up.

The key innovation is using CO2 emissions from cement production as a feedstock for petrochemicals - an integrated and cross-sectoral approach. C2PAT also demonstrates a circular economy approach in the cement and chemical sector given that renewable based plastics can be recycled and reused in various recycling streams. The ‘cherry on the cake’ in this CO2 cycle is the fact that the main fuel in the Mannersdorf plant is already waste plastic. The CO2 it emits is then captured and converted back into plastic!

GC: What is the time-scale for the C2PAT project?

JK: A demonstration plant to capture and process 10,000t/yr of the plant’s CO2 emissions is currently in the planning and engineering phase. It will be in operation in 2024. This stage will generate new know-how to achieve the next step, a full-scale plant capable of converting almost all of the Mannersdorf plant’s 0.7Mt/yr of CO2 emissions into renewable- based hydrocarbons. We anticipate this will be operational by 2030 at the latest.

GC: Could the C2PAT hydrocarbons be used in the cement kiln?

JK: Hydrocarbons, produced from our plant’s CO2, could be refined into any fuel, potentially one for a cement kiln. However, in the net zero-CO2 future it will make sense to replace those fuels that are most difficult to decarbonise, such as kerosene for aircraft.

GC: Why was this plant chosen for this project?

CE: The Mannersdorf plant was chosen for the C2PAT project because it has a long track record of very high-level and increasing technical performance. We had shown that the plant would handle the project well and extract the most value for the wider group. The workforce is very proud that their plant has been selected. It is a testament to their hard work and expertise.

GC: What is the biggest challenge for C2PAT?

JK: I would say that the biggest issue is that decision makers, at both the national and European levels, need to understand the urgency to provide high capacities of renewable energy sources, e.g.: wind and solar. In the longer term Europe’s power will need to come from large photovoltaic farms in the south of Europe and wind power further north. There have to be systems to transport the resulting power itself or the renewable hydrogen, as well as exhaust CO2, with places to store all of these things.

There are also issues around accelerating the permitting process. For example, if you decide today to build a wind farm in Austria, the earliest you can start is 2029. There’s also the NIMBY effect. Everyone wants to sign up to a renewable power tariff, but nobody wants wind turbines in their back yard!

There also needs to be further development of the market for low-CO2 cement products. We would argue that this should include an EU-wide legislation that promotes the use of such products, e.g. starting with public construction projects.

We need to get on with this! I always say there are three decades to 2050, the year by which LafargeHolcim wants to achieve net-zero CO2 emissions. The 2020s are for demonstration, the 2030s will be for scale-up and the 2040s will be for wider roll-out.

Markets and Future

CG: Where are the plant’s main markets?

CE: Mannersdorf plant is located 40km south east of Vienna, which is our main market. We also supply Lower Austria, Austria’s largest Federal State. We also export cement to Hungary and Slovakia.

GC: How were the plant’s markets affected by the Covid-19 pandemic?

CE: Although Austria has experienced several lockdowns, there has been only a minor impact within the Austrian construction industry, our core market. The plant has been able to run almost uninterrupted. We lost two weeks of sales in spring 2020 but after that, sales took off like a rocket. We produced just shy of 1.2Mt over the course of the year.

At the plant level, we offer lateral flow tests on Monday and Friday for all staff, which come back with results in 30 minutes. Such tests provide early detection of the virus and guard against widespread outbreaks.

GC: How have the recent changes to the EU ETS price affected the plant?

CE: The rising ETS price, which hit more than Euro40/t in March 2021, only serves to accelerate our decarbonisation efforts, as well as challenge our cost structure. The main focus areas are thermal efficiency and state-of-the-art production facilities for a CO2-reduced product portfolio and circular economy.

GC: What are your current expectations for the market in 2021 and beyond?

CE: Although the European Commission is forecasting the second weakest economic growth in the EU for Austria, we are cautiously optimistic. There are some infrastructure projects in the pipeline, including several tunneling projects and the expansion of the Viennese Underground. Our major customers signal well filled order books.

GC: What is the biggest challenge for the plant over the next five years?

CE: There are several big challenges for our plant in the near future. One will be how the EU ETS price develops in the future. We continue to work on a CO2-reduced cement portfolio in order to achieve our sustainability goals. Sustainable cements will be more expensive. Our customers will have to take this into account in the longer term. The next big challenge will be the low availability of mineral components and additives, which is already noticeable due to stagnating production of our suppliers, for example the steel industry. Of course, we are also noticing a strong trend towards other building materials, such as wood, in the sustainability discussion. It’s up to us, to position concrete in sustainability schemes like BREAM, LEED, DGNB, etc. in the right way so that the inherent advantages of the product can be conveyed to as wide an audience

as possible.

GC: What is the biggest opportunity over the same time-frame?

CE: This is, for sure, the C2PAT project. With the realisation of the full-scale plant by 2030, we will be able to almost eliminate CO2 emissions from the plant and reposition CO2 as a valuable raw material.

GC: Thank you for your time today.

CE: You are very welcome indeed.