Cement and concrete have built the modern world, but there are signs that the ‘golden age’ of Ordinary Portland Cement is either coming to an end - or is already past. The ‘cement’ industry is now evolving into a different beast entirely, either while seeking the headlines, or avoiding them.

This article attempts to determine if we have already moved past the moment of ‘peak clinker,’ even if we are yet to arrive at ‘peak cement.’ I’ll also give an indication of how I believe the cement industry is ‘secretly’ changing its business model, to cope with the threats and opportunities coming its way.

I’ll start by looking at another industry that shares some of the same problems as the cement industry: Oil. The global hydrocarbons industry has been in the sights of environmentalists for decades. It hits the headlines. We experience its highs and lows every time we fill up our cars with petrol, or ‘gas.’ The global hydrocarbons industry (coal, lignite, oil and natural gas) is undoubtedly first in the sights of government when it comes to action on climate change, but the cement industry will not be far behind.

Peak oil is the theoretical year when the maximum rate of extraction of petroleum is reached, after which it enters terminal decline. Global hydrocarbon reserves are at the highest level they’ve ever been, at around 1.7 trillion barrels, although they have been at that level for a few years - the reserves are not getting bigger.

At current rates of oil consumption, we have 47 years of oil left, although the fact is that global oil consumption is increasing every year, suggesting that the time when the tank is finally empty will be even sooner.

However, the concept of peak oil may now be redundant, with the possibility that the oil will be obliged to remain where it is, and that it will be illegal to extract it - at any cost - due to global warming.

It is already known that there is about three times more fossil fuel in known reserves that could be exploited today than is compatible with keeping the Earth within a 2°C temperature increase.1 Depending on the energy mix, it is suggested that ‘a third of oil reserves, half of gas reserves and over 80% of current coal reserves should remain unused from 2010 to 2050 in order to meet the target of 2°C.’

The first corollary of this is that the oil companies are hugely over-valued, since they will not be able to monetise their reserves. Their share prices do not yet fully price-in the reduction in their future fossil fuel businesses.

A second implication is that their business models needs an update, since they may eventually be legislated out of existence. Many oil companies are making efforts to pivot to a non-fossil-fuel future, by investing in alternative and renewable sources of energy. For example, Total spent about 3% of its total capital expenditure on investments in alternative energy in 2019, with plans in place to ramp that up to 20% over the next 20 years.2 BP has recently been criticised for not spending more on moving away from fossil fuels towards a more sustainable business model, while Shell has been taken to court over its slowness to invest in non-fossil fuels.

Staying with oil, we have seen the first moves by governments to voluntarily curtail any future expansion of the industry - and indeed even to shrink it. Denmark has abandoned any North Sea oil exploration licensing rounds, and has pledged to stop hydrocarbon production from its territory by 2050. The country is a small producer, and its production is already declining, but it is showing the way that other states may follow. The invasion of Ukraine by Russia has temporarily reversed the trend, with European and other governments desperate for domestic sources of energy (hydrocarbon or not), but once the current war in Ukraine is resolved, the fossil fuel industry will once again be out of favour. Eliminating entire CO2-intensive industry sectors is a key lever by which governments will achieve their pledges of ‘carbon neutrality.’ So, three key trends are already in evidence in the oil industry:

- Plentiful reserves that cannot be used;

- Legislative extermination;

- Overvalued companies that need to radically adjust their business models, or die.

My contention is that the cement industry faces the same existential threats as the oil industry, with a vitally important difference.

Cement’s CO2 burden

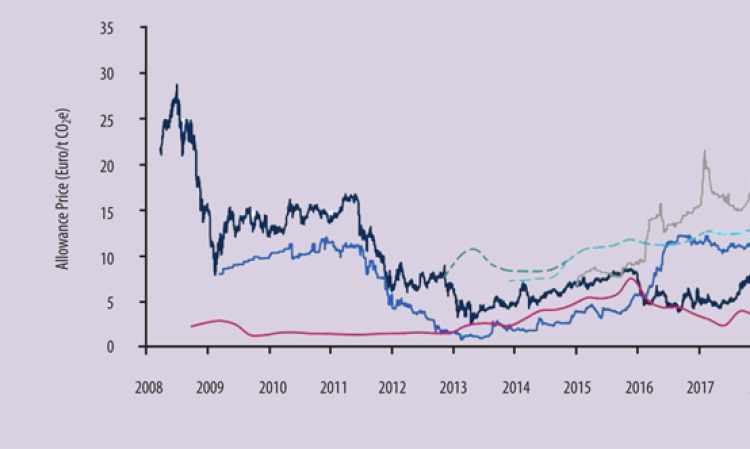

The price of CO2 emissions permits in the EU Emissions Trading Scheme (ETS) has steadily increased from around Euro30/t in October 2020, to hit Euro80/t by the end of 2021, where it has stayed ever since. There is no clear sign of a ceiling for the price at the moment, while future forecasts suggest a CO2 price of beyond Euro100/t by 2030.

According to a recent report3, there are currently 28 ETSs and 29 CO2 taxes implemented or scheduled for implementation at the regional, national and subnational level, covering 11 GtCO2e (around 25% of global GHG emissions). Another report, entitled ‘The Future of Carbon Pricing in the UK’4 but actually looking at global emissions trading schemes, points out that emissions trading schemes are currently also under consideration in Brazil, Chile, Japan, Pakistan, Philippines, Taiwan, China, Thailand and Turkey, and in New Mexico, New York City, North Carolina, Oregon and Washington in the USA. India - the third largest emitter of CO2 - is conspicuously lagging in establishing a CO2 emissions trading scheme. Despite that fact, ETSs are clearly spreading worldwide, since the first was set up in the USA - for SOx - in the 1990s.

The same report4 states that emission permit costs range from US$1/t CO2e to US$127/t CO2e. Figure 2 shows the trend in CO2 emissions permits in a variety of jurisdictions - the clear trend is inexorably upwards. This should be no surprise: Governments have made a lot of promises about their future emissions reductions targets, and now they have to deliver. Their respective ETSs are the main means by which they will pressure their domestic industrial sectors to reduce the specific amount of CO2 produced per unit of output.

The increased costs of production will obviously be passed on to consumers. In the majority of cases the person who foots the final bill is you and I, through our taxes, which go into funding public works, and through any works that we fund ourselves, for example by buying a house. Through the cost mechanism, we will be obliged to consider the CO2 emissions that are involved in the formation of our preferred building material.

Clinker-based cement is the main cementitious binder option for making concrete, but there are other options. In turn, concrete competes against many other materials including wood, steel, bricks and glass. Each has its own CO2 cross to bear - and in the future, its own CO2 bill. The price of CO2 emissions will also eventually be reflected - as it will for cement and concrete - in the price of wood, steel, bricks and glass, and their relative costs and properties will be taken into account in deciding which to use.

The fact is that cement is just one of the multiple ingredients in concrete. Less cement will be used in concrete in the future, and furthermore, the amount of clinker - specifically Ordinary Portland Clinker, OPC, the highest-CO2-emitting clinker type - that is used to make cement will also drop.

We already have far too much clinker production capacity around the world - very few countries are now obliged to import cement or clinker (the US being an obvious exception). The majority of the excess capacity is in China, but the Chinese are taking tough steps to retire excess capacity. In December 2020 it was reported5 that the Chinese Ministry of Industry and Information Technology (MIIT) released tougher draft rules regulating how cement producers should decommission old production capacity before they build new capacity. Under the new guidelines, cement companies must retire at least 2t/yr of outdated capacity for each 1t/yr of proposed new capacity, in areas classified as environmentally sensitive. Previously, the ratio was 1.5:1. In non-environmentally sensitive areas, at least 1.5t/yr of obsolete capacity should be retired for every 1t/yr of new capacity, an increase from the previous ratio of 1.25:1. China is already past ‘peak cement,’ and its production capacity will inexorably drop in the coming years - as has already been the case with a number of developing nations, particularly in Europe. Although accurate numbers are very difficult to come by, I feel that the world may already have passed the moment of peak clinker production.

As mentioned previously, governments are seemingly intent on pricing CO2 emissions to encourage reductions. However, there may be an alternative model for curtailing CO2 emissions: an outright ban on the emission of gases which harm the environment, potentially including methane and CO2, at any price. If you think it can’t happen, then think again, because it already has, albeit for different gases. The Montreal Protocol banned the production, use and emission of Ozone Depleting Substances, including CFCs, to stop the growth of the Ozone Hole over Antarctica.6 If such a ban on the production of CO2 was to be enacted, this would make future business for the cement industry very difficult indeed - Unless the industry either finds itself low-or-no-CO2 alternative ‘cements’ (which it is working hard to do) or an entirely different alternative business model.

How the industry is ‘secretly’ changing

The first half of this article looked at the ‘why’ of change in the global cement industry, and now the second half will look at the ‘how’ of change. At the IEEE-IAS/PCA Cement Conference in Las Vegas in April 2022, I gave a presentation7 on how I believe the cement industry is ‘secretly’ changing. In fact, it is not so secret - Holcim trumpets its ‘Accelerating green growth’ agenda on pages 2 and 3 of its 2021 integrated annual report. However, Holcim apart, the other major multinationals are a little ‘coy’ about how far and how fast they are changing their core business models.

The major multinationals stampeded into Asia in the late 1990s, to buy-up as much growth potential as they could while the Asian Tigers were growing at their fastest. They doubled-down on their investments after the Asian Financial Crisis of 1997, sensing that bargains were to be had. This resulted in the mainly European cement majors (and Cemex) owning large chunks of the Asian cement industry in the early 2000s. However, these investments came with big debts, and the price of servicing those debts - particularly when conditions deteriorated in the West after the crisis in 2008 (the greatest recession for 80 years, don’t forget) became ruinous (especially if you had overpaid for the assets, as Cemex did for Rinker in 2007). The pendulum swung the other way, and the 2010s have seen an accelerating stampede out of Asia, as cement companies have realised that there are more stable returns to be had elsewhere (most particularly in Europe and in the US). As Albert Manifold, CRH CEO, said in an Earnings Conference call in August 2019, “You’re faced with a capital allocation decision of investing in Europe or North America where you’ve got stability, certainty, overlap [and] capability, versus going for somewhere a bit more exotic [BRIC countries, developing world]. The returns you need to generate to justify that higher level of risk are extraordinary and we just don’t

see it.”

As well as a rebalancing of their geographic spread, the multinationals are continually rebalancing their business portfolios. Nearly every cement company has either organically grown and/or bought assets to grow an aggregate business and a concrete business - in the classic vertically-integrated cement-aggregates-concrete business model.

Increasingly though, in the last couple of decades, many cement business have grown organically, developing their own new side-arms including in waste management and alternative fuels production, procurement of supplementary cementitious materials (SCMs) and fuels, shipping and logistics arms, electricity production through captive power generation, solar and wind farms and waste heat recovery, and making the most of their raw material resources through the creation of lime and agricultural lime divisions. These ‘attractive adjacencies’ make up a ‘vertical integration plus’ business model, which has been adopted by both multinationals and smaller ‘cement’ companies around the world.

As well as growing their businesses, the multinationals commonly buy and sell (or even swap) companies and assets in order to rationalise and optimise their portfolios. It is in this area that I think that the cement companies are currently most active in reshaping their businesses (or not, as we shall see).

Holcim: turning the supertanker

Returning to Holcim, we can see that with the appointment of Jan Jenisch as CEO in 2017 there has been a marked pivot in the company’s direction. Between 2012-17, Jenisch was the CEO of Sika - a Swiss multinational company very active in construction chemicals. According to Holcim, when Jenisch joined the company, he ‘committed himself to making Holcim the global leader in innovative and sustainable building solutions.’ He has certainly already done that, expanding the company’s Solutions & Products business with a number of major acquisitions.

Holcim’s recent major acquisitions (and divestments) give us a signpost on where the company is heading in the future. It has recently bought Firestone Building Products (flat roofing) in the US; Malarkey Roofing Products (US); PRB Group (coatings, insulation, adhesives and flooring) in France; PTB-Compaktuna (additives, Belgium); Izolbet (insulation, construction chemicals, dry mortars, Poland); Cantillana (façade construction systems and external thermal insulation composite systems, Belgium); and SES Foam LLC (spray foam insulation, US), adding them to its ‘Solutions and Products’ division. Holcim has also added a large number of aggregates, concrete and asphalt businesses too. Concurrently, Holcim has divested itself of very large tonnages of clinker production capacity, selling its cement businesses in Brazil (to CSN-Companhia Siderúrgica Nacional for US$1.025bn); exiting the Russian market (after Russia’s invasion of Ukraine); its business in Zambia for US$150m; selling Cookstown Cement in Northern Ireland; and selling its Ambuja Cement and ACC cement businesses - with 31 integrated cement plants - in India to Adani for around US$6.5bn.

It is important to note that these deals will have taken some time to put together, and that there are certainly many others in the acquisition and divestments pipeline. Holcim is like a supertanker - its size means that it will take some time for it to change course for an entirely new direction. However, Holcim’s own numbers show us the near-term destination: From cement accounting for 60% of its revenues in 2020 (and Solutions and Products (‘S&P’) only 8%), by 2025 Holcim is aiming for S&P to make up to 30% of revenues, with cement accounting for only a little more, about 35%. By then, Holcim will not really be a ‘cement’ company any more: it will have four core areas - cement, S&P, aggregates and readymix. Jan Jenisch will not stop there though and we can expect to see a steady diminution of the CO2-intensive cement part of Holcim’s portfolio beyond 2025.

The company’s previously high-CO2-intensity business model may have dented its share price in an increasingly CO2-aware world. We can expect the ‘pivot’ to boost the value of the company as it turns towards producing more sustainable building products. It is purchasing these alternative building material assets at a relatively early stage in this trend, before their price is artificially inflated by scarcity (in a reflection of big oil companies now chasing increasingly expensive low-CO2 energy companies to buy).

Cemex seeks new direction

Mexico-based Cemex is also turning the supertanker. In its own words, the company is seeking attractive, bolt-on investment opportunities, is constructing a portfolio more weighted to the US and Europe, is focusing on vertically integrated positions in attractive metropolises, is undertaking strategic divestments to streamline its portfolio and to de-leverage, and it will develop its Urbanisation Solutions (‘UB’) division as a core business. UB only started in 2019, but already makes up 8% of Cemex revenues, with the Cemex Admixture business as its heart. However, UB also includes insulation, recycled aggregates, alternative fuels and waste management amongst its business activities. UB had a revenue of US$1.9bn in 2021, and EBITDA growth of 22% - it is already big, and it is growing fast. Cemex also has a very active ‘Cemex Ventures’ business, which is involved in corporate venture capital, particularly in the technology sector, and it has built one of the largest virtual sales organisations in its Cemex Go platform. Taken together, these moves give the impression of a company urgently trying to innovate itself away from its previous core businesses.

CRH

The former Cement Roadstone Holdings has already started its own pivot away from ‘exotic’ locations towards more developed markets such as Europe and the US (see above). However, in common with Holcim and Cemex, the company is also intent on growing its own alternative ‘Building Products’ business, which currently makes up around 26% of revenues and employs 23,500 people in 510 locations in 19 countries worldwide. The business comprises architectural products including pavers, blocks and kerbs, retaining walls and slabs; infrastructure products, including precast concrete, PVC and polymer-based products; and construction accessories, including anchoring, fixing and connection solutions, lifting systems, and formwork accessories. CRH sold its architectural glass business to KPS Capital Partners for US$3.8bn in 2022, no doubt freeing-up cash to invest in new acquisitions and paying down debt. CRH is intent on growing its portfolio of sustainable products to 50% of its revenue by 2025 - it is another company that is pivoting towards lower-CO2 products.

Heidelberg Materials - Late to the party?

Heidelberg Materials, which changed its name from HeidelbergCement in September 2022, used to be unique among the major manufacturers in that it had ‘cement’ in its name. This is no longer the case. However, Heidelberg Materials is still notable for its apparent ‘doubling-down’ on its cement production business in the face of high energy costs and rising CO2 prices which have impacted on its share price. It has unarguably become a world leader in reducing specific CO2 emissions from its cementitious products, leading in alternative fuels, low-CO2 cements, lower clinker concrete, electrification and CO2 capture. The company seems to be concentrating on CO2 reduction from its current cement business, rather than undertaking a wholesale portfolio optimisation or redirection into attractively-adjacent lower-CO2 building materials, although its name change indicates that a transition is now more likely.

However, speaking of the change, Heidelberg Materials’ Managing board chair Dominik von Achten said “We are proud of our cement business, but the company’s range of services goes far beyond cement. Today, and even more in the future. Our future is sustainable. Our future is digital. Customer demands, markets and competitors are changing rapidly. Opportunities and challenges go beyond country borders; communication is becoming increasingly global.”

Other companies turning too

We could continue with a roster of cement companies that are looking at ‘attractive adjacencies’, not just in the ‘vertical integration plus’ model that was mentioned above, but into insulation, roofing, chemicals, wallboards, cement-boards and prefabrication, to make a horizontal integration model, as well as using their distribution, logistics, sales and channels to market. Votorantim Cimentos for example has recently acquired businesses in cement, concrete, aggregates, mortars, grouts, finishing products and plasticisers, logistics and distribution, agricultural lime and waste management and is expanding its wind and solar power involvement. Chinese cement companies are increasingly looking at diversification strategies, away from a saturated and increasingly unprofitable Chinese cement market.

Some companies will be better able than others to take advantage of market opportunities. The level of debt leverage varies across the industry, with Holcim, CRH and Heidelberg Materials all currently in healthy financial positions, ready to pounce if ‘attractive adjacencies’ come up for sale.

Conclusion

The world is saturated with CO2-intensive clinker, and the price of emitting that CO2 is likely to increase. Savvy companies are either pivoting away from traditional cements and are building non-cement businesses, or are ‘betting the farm’ on reducing CO2 from traditional processes (and new cements). In the future, it is likely that all of today’s ‘cement’ companies will take both approaches.

References

1. McGlade, C., Ekins, P. ‘The geographical distribution of fossil fuels unused when limiting global warming to 2°C, Nature 517, 187–190 (2015). https://doi.org/10.1038/nature14016.

2. https://www.nsenergybusiness.com/features/oil-companies-renewable-energy.

3. https://www.theccc.org.uk/wp-content/uploads/2019/08/Vivid-Economics-The-Future-of-Carbon-Pricing-in-the-UK.pdf.

4.https://icapcarbonaction.com/en/?option=com_ attach&task=download&id=726.

5. https://www.globalcement.com/news/item/11774-ministry-of-industry-and-information-technology-toughens-chinese-cement-production-capacity-reduction-rules.

6. https://en.wikipedia.org/wiki/Montreal_Protocol.

7. McCaffrey, R. ‘How the global cement industry is secretly changing,’ Presentation at the IEEE-IAS/PCA Cement Industry Conference, Las Vegas, 2022.