Jagdeep Verma provides a detailed overview of India's cement sector, the second-largest in the world, and one that still has high potential for growth.

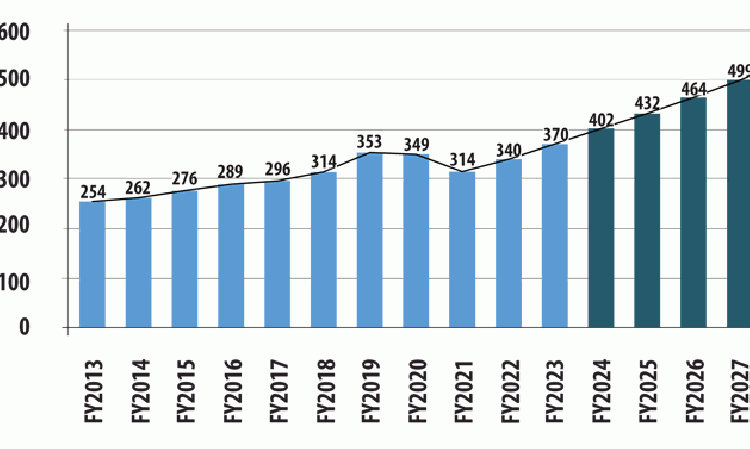

Cement demand in India fell by 10% year-on-year in the 2021 financial year (FY2021) due to the Covid-19 pandemic, with demand dropping to the same level as in FY2018 at around 314Mt (Figure 1). Demand bounced back with growth of 8% in FY2022 to reach 340Mt, and then by 9% in FY2023 when it reached around 370Mt. Demand is now envisaged to grow between 6.5% to 8.5% per year over the next 5 - 7 years, reaching 535Mt in FY2028 in the most likely scenario.

Cement capacity

India had an installed cement capacity of 595Mt/yr at the end of FY2023, with around 80 producers operating 300 cement facilities. Of these, 170 are integrated, and 130 are grinding plants, blending units and terminals. However, the top 25% of producers - either major Indian producers or regional players - hold about 85% of the total capacity.

India is expected to add around 120Mt/yr of additional cement capacity over next five years. This means that the total installed cement capacity will reach an estimated 700Mt/yr by FY2028. Another 150Mt/yr is believed to be at the planning stage within the top 4 - 5 players. In the eventuality of this additional capacity also materialising, the nation's cement surplus would increase substantially and continue to lead to lower return on capital.

Supply and demand balances

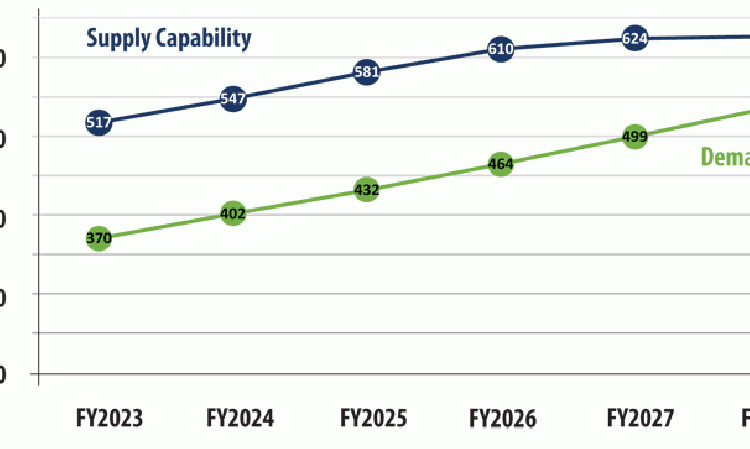

The effective cement capacity / supply capability (which is calculated from the installed capacity assuming that all of India's cement plants can operate at a maximum of 90% capacity utilisation, and considering operational capacity of the plants that came up during the year) was about 515Mt/yr in FY2023. It is expected to reach about 625Mt/yr in FY2028.

Regions

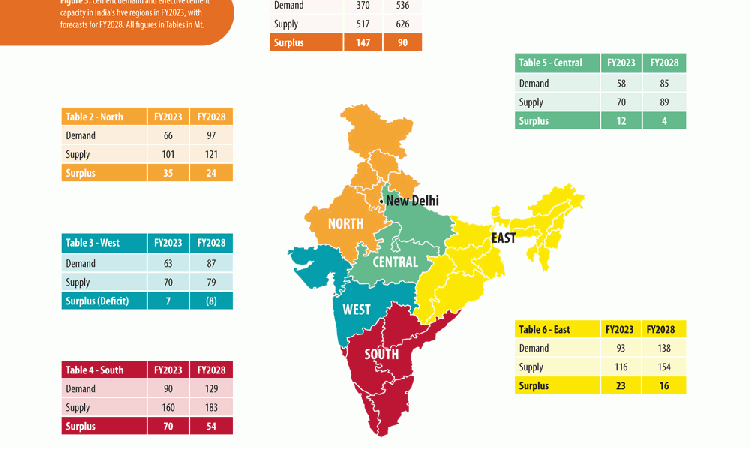

India is divided into five regions when discussing its cement industry: North, Central, East, West and South. Cement demand is highest in the East region, whereas the South region has the highest cement capacity. All regions have surplus cement. However, by FY2028, the West is envisaged to transition to a deficit, while the Central region is expected to have only a marginal surplus (Figure 3).

This does not necessarily mean that plants located in regions with higher surplus have lower capacity utilisation, as there is inter-regional movement of cement. For example, plants in the North region supply cement to markets in Central and West regions. Plants in the South similarly supply cement to the East and West.

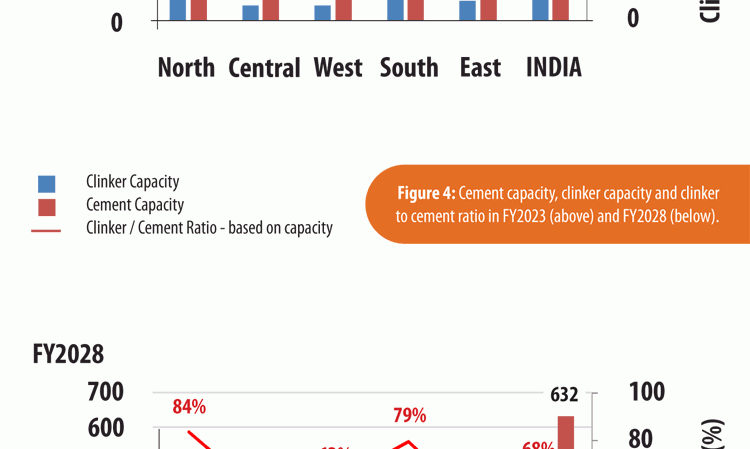

The distribution of capacities in the country can be better understood by looking at the clinker and cement capacity at the regional level. In FY2023, the clinker capacity of India was around 380Mt/yr, enough to produce ~535My/yr of cement, whereas the rated cement capacity was 595Mt/yr and the effective cement capacity was about 525Mt/yr. This implies that, at the country level, there is adequate clinker for the effective capacity to work at 100% utilisation.

In FY2028, the clinker capacity of the country is expected to be 427Mt/yr, such that it can produce about 615Mt/yr of cement, whereas the rated cement capacity will be 700Mt/yr and effective cement capacity is about 630Mt/yr.

Clinker and cement capacity is highest in the South region mainly due to higher availability of limestone. Clinker capacity is lowest in the Central and West regions, and grinding units located in these regions also receive clinker from North and South regions.

Holtec Consulting's analysis of cement demand, effective capacity, market product mix, and other factors shows that:

1. Only the West and East were clinker deficient in FY2023. Grinding units in these regions get clinker mostly from the South;

2. In FY2028 the Central, West and East regions are expected to have net clinker deficit, likely to be fulfilled from the South and North;

3. The cement ratio (capacity based) in FY2028 will be the lowest in the East due to a higher focus on producing blended cement. It will be highest in the North and the South due to a potential lack of supplementary cementitious materials in these regions.

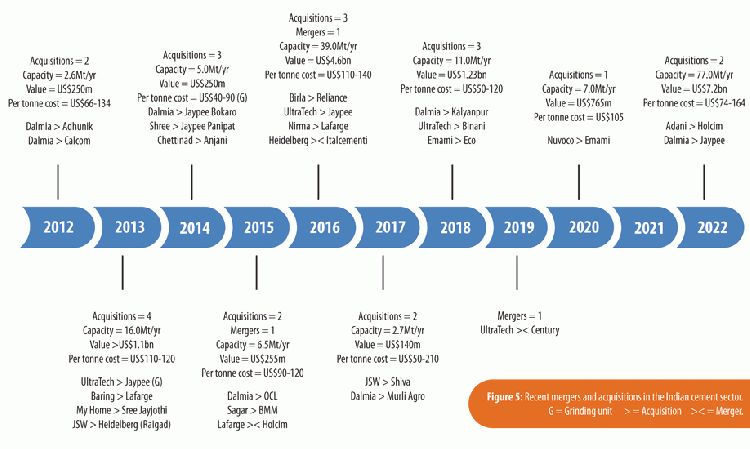

Consolidation

Industry consolidation is commonly measured using the Herfindahl Index (HI), where 0 indicates perfect competition and 1 indicates monopoly. Industry consolidation in the Indian cement industry is low, with HI of <0.10.

Around 165Mt/yr of cement capacity has changed hands within the Indian cement industry in the past decade (Figure 5). The value of the acquisitions was approximately US$15.8bn. Significant merger and acquisition potential remains in the industry, with major companies competing to enhance their capacity share by adopting both organic and inorganic growth strategies. On the other side, several companies that are under financial strain are looking to exit the business. The enterprise value for future mergers and acquisistions is expected to be in the range of US$110 - 130/t of cement capacity.

Product mix

India is predominantly a blended cement market, with 70% share of blended cements and 30% OPC. The supplementary cementitious materials (SCMs) currently used in India are mainly fly ash and slag. Fly ash is available across the country, whereas slag is available mainly in the East and parts of the South.

As per the Bureau of Indian Standards (BIS), Portland Slag Cement (PSC) can be manufactured using a maximum of 70% slag. Portland Pozzolana Cement (PPC) can be made with a maximum of 35% fly ash and Plain Cement Concrete can be produced using 20 - 50% slag and 15 - 35% fly ash. The balance is clinker and gypsum. The percentage of gypsum depends upon the required setting time, but is typically less than 5%. The BIS has also recently established specifications for Portland Calcined Clay Limestone Cement, which comprises 50 - 80% clinker, 10 - 35% calcined clay, 5 - 20% limestone and gypsum as required.

In the future, the clinker to cement ratio is expected to shift from the current 72% to around 68% by FY2028, indicating a general increase in the use of SCMs.

CO2 - A growing concern

Table 7 - Indian Cement CO2 Emissions

| kg CO2 / t cement | |

| Raw materials | 360 |

| Thermal fuels | 200 |

| Electrical power | 70 |

| Transport to market (500km average) | 20 |

| TOTAL | 650 |

CO2 emissions from cement production are estimated to be ~8% of India's total emissions, around the global average. The emissions from each stage of the process are shown in Table 7. As elsewhere, Indian cement producers are becoming increasingly aware of their CO2 footprints. Many are working towards reducing emissions, despite the fact that India already operates many of the most modern and energy-efficient plants in the world. Typical approaches include alternative fuels, renewable electrical power, futher improvements to energy efficiency and waste heat recovery (WHR) systems. Producers are also working to increase the circularity of their products, including via increased production of blended cement products, recycling old concrete and CO2 capture, utilisation and storage (CCUS). The government is also considering the introduction of stricter controls for various pollutants.

Final thoughts

Limestone, fossil fuels and water resources are becoming scarce, including in India. Given this, limestone auction prices are envisaged to remain high, with low clinker-to-cement ratio products, alternative fuels, alternative raw materials and mitigating CO2 emissions all expected to further gain importance. Improvements in energy efficiency and equipment availability have been the major focus areas for cost reduction in India in the past. In the coming years, the focus on cost optimisation will be higher, both within the production and distribution activities. There is also potential to reduce costs in non-equipment related domains, for example material inventories, consumable consumption rates, financial expenses and so on.

Indian cement demand is likely to surpass effective supply in the next seven years. With increased gestation period and some recent mergers and acquisitions, major cement players are likely to continue to increase their capacity to ensure their capacity share improves or - at least - is not adversely impacted in the future.

At present the effective capacity utilisation is ~70%. This is likely to start improving if there is no race for inordinate capacity build up. Opportunities will continue to exist for acquisitions in the cement sector, albeit at a reasonable valuation of probably US$110 - 130/t of cement capacity. In the short term, the focus will be to increase earnings before interest, tax, depreciation and amortisation back to 'pre-fuel hike levels' and thereby improve return on capital in the cement sector.

Jagdeep Verma

Jagdeep Verma is the Head of Business Consulting at Holtec Consulting, a premier cement consulting firm. His career spans more than 25 years, during which he has led around 300 multi-functional consulting assignments for over 80 clients in

more than 30 countries.