This article is the third in a series of four to look at major trends in the global cement sector over the past 40+ years, this time focusing on the ‘morning after’ the 1990s cement ‘party.’

1 Technology and operations

Cement, aggregates and concrete companies entered the New Millennium in good health, or so it seemed. The demand curve continued to rise in the vast majority of countries. Global trade in cement had never been higher and even prices were rising. If producers decreased their clinker to cement ratio, it was mostly to stretch out limited clinker to make more cement to sell.

In the early 2000s the industry was cash rich and capital expenditure was plentiful. Mergers and acquisitions were vibrant. There were also many plant modernisations, with higher clinker demand the main driver. The returns on those projects were not always impressive, but apparently justified given the ‘perceived permanency’ of plants operating at >90% capacity utilisation rates. Strategists’ warnings that ‘past performance is no indication of future success’ had started to sound like a boring uncle cautioning the younger generation not to party too hard. Companies were more interested to see if they could break their own production records than worrying about future customer needs and demand trends.

However, new technological advances had slowed to a snail’s pace. Plants stretched beyond their design capacity were squeezing out every last tonne of cement they could. This performance was helped by higher quality wear-resistant materials, lubricants and refractories and advanced IT solutions for maintenance and condition monitoring, which had moved the bar on reliability. Previously unheard-of mean times between equipment failures of >400hr were not uncommon.

By that point, European equipment manufacturers dominated the global project scene, as US suppliers had fallen by the wayside in the 1990s. However, this too was changing. Having grown capacity in China with extraordinary speed, Chinese plant suppliers turned their attention to the global stage. Their offers were largely based on five-stage precalciner kilns with flexibility to incorporate several key European components like vertical raw mills and grate coolers. The advantages of this approach were not only that the design had been thoroughly refined through multiple iterations in China, but that the capital cost was lower. This reduced barrier to entry rapidly broadened the base of owners in the cement industry. Capacity was built in places that had no prior local supply, often by investors who were new to the sector.

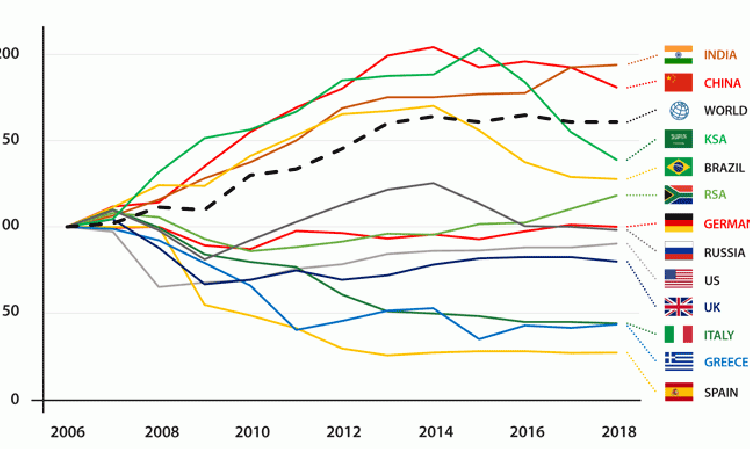

And then came the crash of 2007 - 2008. The global effects on the cement industry were very mixed. While it is popular to look at Western markets as ‘typical,’ it is not the case that cement production ‘tanked’ globally. Indeed, production of cement rose by more than 60% between the pre-crash peak of 2006 and 2018 (Figure 1). While many developed economies did see clear nose-dives, China and India both made nearly twice as much cement in 2018 than they did in 2006. Brazil, Russia, Saudi Arabia and South Africa all saw differing trajectories, while many smaller markets not shown here are likely to have seen growth ‘off the chart’ due to their low 2006 bases.

The most pressing need in developed markets was to ‘unlearn’ the lessons of the party years. The nimblest companies immediately cut maintenance expenditure and operating expenditure to a bare minimum. They cancelled most major projects and had to work out how to run kiln campaigns at 50% capacity. For multinationals, the mindset from developed markets was often carried through to their other operations.

For everyone, the Darwinian principle of ‘survival of the fittest’ meant that many smaller plants and those with outdated technology soon closed. Fixed costs were an enemy that had to be beaten. For everyone, new technology was put on the back burner - literally - as the only investments that survived were for alternative fuels. However, this was not universally the case. In Asia new plants, using the now standard technology from China, continued to be built, even where the local industry was already running at low capacity utilisation.

2 Energy, emissions, alternative fuels / materials

The use of petcoke and cement production had marched in lockstep in the 1990s, a trend that continued in the early 2000s. The use of spongecoke, as well as the lower cost but more challenging shotcoke, had steadily developed for both kilns and precalciners. The upside to petcoke was that it was generally at a lower cost per GJ than coal. However, this discount could change rapidly between 75% at best to virtually zero at worst. The downside for the cement industry was the high sulphur content and difficult combustion characteristics due to the low volatile content compared to coal. However, energy companies needed petcoke to be used by the cement industry as much as the cement industry needed petcoke. Usage continued to rise.

Petcoke sources also changed. In 2000 global petcoke production was ~55Mt/yr, with 65% produced in the US. By 2010 production was 95Mt/yr, with 50% from the US. By 2018 the volume was 135Mt/yr, with less than 40% from the US.

China, India and Saudi Arabia had changed the dynamic. Greater competition at lower logistics cost made petcoke prices very attractive. The pressure was on plants to take advantage of this economic benefit. Plant modifications with new high momentum burners, upgraded coal mills for finer petcoke grinding, precalciner extensions and preheaters festooned with air cannons - and complaints about dusty clinker - all followed. From 2000 to 2018 the ability to switch between coal and petcoke depending on price per GJ was a key performance metric.

In contrast, the transition to alternative fuels continued to challenge the cement industry, with modest global growth. Until 2007 capital expenditure for alternative fuel projects was plentiful, but many of the alternatives caused kiln production to fall. This was highly undesirable from 2000 to 2007, when 100% clinker production capability was generally needed. The industry wanted cheap alternative fuel, but cheap fuels were often of variable quality, with high moisture and ash content.

Even after the 2007 economic crash, alternative fuels failed to find global traction, albeit with some notable exceptions like Germany and Austria. The issues were manifold. A lack of organised waste collection and processing, lack of landfill taxes, local resistance due to environmental fears and high cost equipment were just a few of the barriers.

The Kyoto protocol, signed in late 1997, finally marked a more universal approach to global warming and CO2 emissions from governments around the world. This was an impact that would grow and grow. Rather than rely on direct limits to CO2 emissions, the initial government choices - depending on the country - were either to follow the fiscal route or, frequently, to do nothing.

The most significant of the early methods was the EU Emissions Trading Scheme (ETS) cap and trade concept, which finally saw the light of day in 2005. As a classic example of unfortunate timing, the initial free allowances of the ETS were calculated during the output boom of 2002-2004. During the crash of 2007-2009, European clinker production dropped precipitously, which enabled some CO2 allocation trading to add to cement revenues. Perhaps even more importantly, it became apparent that burning petcoke and coke - the highest CO2 generators - would not be sustainable in the long term. Investments in alternative fuels received a boost.

3 Products

Conventional cement standards slowly evolved between 2000 and 2018. The US, having published the performance-based standard ASTM 1157 in 1992 now added ASTM C585 in 2012. ASTM 1157 had been slow to gain construction industry acceptance. The objective of ASTM C585 was to allow a greater volume and variety of additions to cement as an echo of the European EN197 recipe-based systems. Meanwhile in Europe, where climate change was steadily working its way up the ‘to do’ list, a proposal to include the addition of CEM II/C and CEM VI qualities of low clinker content cements was launched in 2012-13. However, this was not finally enacted until 2021.

As in the cement sector, power generators and steel producers were also in the firing line with respect to their CO2 emissions. These industries provided the cement and concrete producers with valuable fly ash and blast furnace slag. However, just as the need for such by-products was rising, the opposite was happening on the supply side. Beginning in Europe and the US, coal-fired power stations and blast furnaces began to fall in number.

With the increasing attention brought to the fact that the cement industry is responsible for ~7% of global CO2 emissions, it was inevitable that Portland cement and its derivatives, effectively unchallenged as a construction material for 200 years, would finally come up against new contenders for the title. Geopolymer cement had been known about for many years and even launched commercially in Belgium in the 1950s and in the US in the 1980s. Neither made the breakthrough to full commodity. However, a new impetus since 2010 has seen several companies launch geopolymer products. Vertically-integrated companies started to optimise concrete design, work on new chemical additives with their suppliers and - increasingly - invest in full-scale product innovation.

4 Corporate - Models and economies

The industry breathed a collective sigh of relief as the Millennium bug failed to bring its plants to a grinding halt. Preparations for 1 January 2000 had lasted for months and were undertaken by large and often centralised teams all over the world. For many, it prompted the modernisation of IT systems, as well as improvement of some industrial standards and synchronised operating procedures. However, for the industry as a whole the turn of the Millennium signalled a new era. For the first time a single technological threat was no longer limited to the traditional 200km radius of a plant - it could impact operations around the world. For the first time, risk management at the city or even country level would not suffice. It had to be addressed systematically, with careful and rapid collaboration between corporate and local teams.

This illustrates the extraordinary transformation of the global economy and a now truly ‘global’ cement industry, distinct from the ensemble of national and regional industries that we wrote about in the first two articles in this series. It created the opportunities, but also the new challenges and contradictions for the global building material players. An economic problem in one country could now instantly change global forecasts. At the same time, areas such as corporate compliance, health and safety, sustainability in all its forms, developing and maintaining government and public relations - and more, were becoming as important as clinker production.

By the early 2000s the industry arrived at a paradox. Despite some growth in international trade to bridge occasional capacity unbalances, markets were still mainly served by the traditional model of a plant shipping to customers nearby. Product portfolios were mainly small, with OPC by far the most commoditised. On the other hand, more and more technologies for the efficient production and use of building materials had become patented and so the days of local mechanics patching up older plants with hand tools were coming to an end. Also, this capital-intensive industry required significant financial capacity and could not be profitable without some degree of stability and careful long term planning.

The larger corporations had access to capital to execute most ambitious large projects, so it is no coincidence that the first true ‘multinationals,’ companies that operate in 50-plus countries with in excess of 100Mt/yr of cement capacity, emerged by around 2005. They acquired smaller producers, merged and - sometimes - divested strategically.

At the same time, many small, well-disciplined family owned companies continued to succeed and some large state-owned operations also grew. New, fast-growing players periodically emerged, especially in Africa and the Middle East, challenging the status quo. As with equipment manufacturers, US-owned cement producers mostly disappeared, in part through their neglect of energy efficiency and more sustainable technologies. To this day, the multinationals remain in European, Latin American and Asian ownership.

The steady growth of the multinational was halted by the global financial crisis of 2007 - 2009, with its effects still prevalent today. The large volume kilns and use of debt-financing for expansions seen in the 1990s and early 2000s had provided healthy cash generation and long lines of trucks outside the plant when the party was in full swing. Now, in the post-crisis hangover, producers were left with the headache of how to use their capacity fully, with rapidly escalating fixed costs per tonne, falling productivity and all the other ill effects that come with operating a cement plant at <90% of its design capacity soon evident.

This drop off in demand signalled the need to change business model almost entirely. By 2010, much new capacity was out of the question. In the country with the biggest boom - China - ghost cities, unused new airports, unfinished bridges and highways became the new normal. Projects stalled in many other markets, both developed and emerging.

In combination with the now clear need to decarbonise, it had become obvious to industry leaders that the ‘business as usual’ patterns established over the cement sector’s first 200 years was over. Declining - or highly cyclical - demand, pressure to rationalise and reduce plants’ emissions, new demands placed on products from elsewhere in the value chain, a move away from commodity products and - perhaps most importantly - the structural, rather than cyclical nature of each of these changes had fundamentally altered the business of making cement. There was an urgent need for new technologies, products and partnerships... indeed a need for an entirely new philosophy for the global cement sector.

Up next

The next article will explore the past five years and will look to the future, an exciting time in which changes will come thick and fast, transforming our ‘old grey industry’ into one of the most dynamic

sectors the world has ever seen.

Lawrie Evans

Lawrie Evans founded EmCem Ltd, a UK-based cement consultancy, in 2014. He previously worked for more than 40 years at Italcementi, Heracles Cement and Blue Circle in the UK, Greece, the US and Italy across optimisation, management, operations and chemical engineering.

Gregory Bernstein

Gregory Bernstein has worked for Holcim for more than 30 years. He met Lawrie Evans in the UK in the early 1990s, before taking on process, project, strategy, well cement and business evelopment roles in the UK, Europe and the US.