The EU Emissions Trading Scheme (ETS) Carbon Border Adjustment Mechanism (CBAM) came into force on 1 October 2023, with full implementation from 1 January 2026. Dan Maleski, Lead CBAM Analyst at Redshaw Advisors, looks at its implications...

At Redshaw Advisors, the advent of the Carbon Border Adjustment Mechanism (CBAM) is something that we have been preparing for since the initial announcement a few years ago. Even with our decades of experience in emissions trading, the extent of the CBAM’s geographical coverage and depth of financial impact means it demands serious consideration. On Sunday 1 October 2023, the first stage of this long-awaited piece of legislation went live. Built into the expansion of the EU ETS, the CBAM is a key tool for making the bloc ‘Fit for 55,’ i.e.: reducing emissions by at least 55% compared to 1990 levels by 2030.

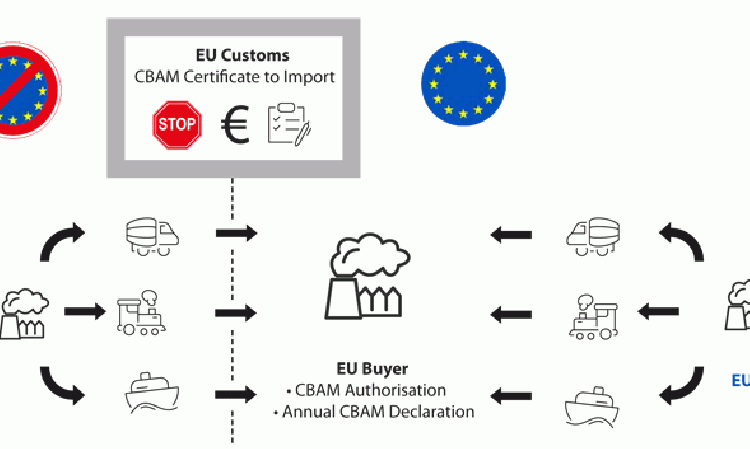

The EU CBAM casts a carbon price onto a wide range of goods imported into the EU to simultaneously prevent European manufacturers relocating to countries with lower environmental standards and prevent companies from being priced out by more polluting goods made in non-EU countries. Within the EU, it is hoped that this mechanism will encourage other countries to reduce the carbon intensity of their processes and / or establish complementary national carbon pricing schemes.

As of 1 October 2023 importers into the EU will have to report the greenhouse gas emissions embedded in goods including iron and steel, aluminium, electricity, fertilisers, hydrogen and – you guessed it – cement. This is for raw, semi-finished and final products. Importers and installations must submit all relevant information to the European Commission’s CBAM database.

How are cement producers affected?

In comparison to other sectors covered by the CBAM, cement producers are at a slight advantage for two reasons. Firstly, the GHG accounting exercise is relatively less complicated as there are fewer variables both in processes and products. The only relevant GHG is CO2, which will need to be measured in metric tonnes (Mt). Secondly, Europe is a net exporter of cement, and is less CO2 intensive in compared to other producers because of the more common practice of using low carbon fuels, waste materials, natural gas and biomass. Nonetheless, the embedded emissions of the following will need to be established:

- Goods: Calcined clay, cement clinker, high alumina cement, as well as different kinds of Portland cement and hydraulic cement;

- Activities: production of clinkers and clays, grinding and blending the clinker, indirect emissions coming from the quantity of electricity consumed.

Different goods will need to take different production process routes and different emissions sources into account. Installations may source energy from producers at other sites - and these will also need to be included as indirect emissions. The web of emissions that needs to be reported can be spun far beyond what is initially expected, which is why Redshaw Advisors presses the need for its clients to communicate with suppliers outside of the EU and assess what information is available now.

Around a third of emissions from cement production originates from the energy consumed in powering the process – there is a real environmental and financial opportunity to use electricity or bio-methane for heat and potentially for capturing and storing the CO2 directly from the kiln. Additionally, renewable power purchasing agreements (PPAs) can be used to account for indirect emissions, which Redshaw Advisors’ clients are already exploring with its renewable energy team. Although the Definitive period for CBAM (See Page 12) seems far away, these emissions’ reduction conversions take time. With sufficient preparation, such changes can be opportunities instead of just costs a few years down the line.

What is its geographical coverage?

In short, global. The main cement exporter to the EU is Türkiye, accounting for a third, with the rest divided between South America and Eastern Europe. Production sites outside the EU will be able to register at the EU central database to communicate their emissions reports. One of the fundamental purposes of the transitional phase is to allow importers and producers ample time to communicate their reporting needs to each other and become accustomed to the centralised database before the Definitive period begins. The cost of the CBAM certificates required to cover the imports will help to determine the economic viability of making processes less polluting.

For those unable to calculate the exact emissions associated with their goods, ‘default values’ available from the European Commission website can be used to account for up to 20% of the product process for complex goods. It is thought that these will likely be higher than reality, meaning there’s an incentive for importers to assist non-EU installations in calculating and declaring genuine, specific data before 2026. Foreseeing the complexity of this process, Redshaw Advisors has been forming partnerships with Measurement, Reporting, and Verification (MRV) and accounting specialists that have international experience.

The European Commission has stressed that the border levy is in line with World Trade Organization rules in that it treats foreign and domestic firms alike and allows any carbon prices already paid abroad to be deducted from the border cost. Nonetheless, many countries which are significant exporters in other sectors, such as steel, have taken umbrage. In 2022 Brazil, South Africa, India and China obliquely called CBAM ‘discriminatory’ and a potential source of ‘market distortion and aggravator of the trust deficit.’ Other impacted countries, such as Australia and India, have since accelerated the development of their own carbon border taxes - although whether this is out of respect for the environmental ambition or in political retaliation is a matter of perspective. Either way, there is impending pressure on industry across the world to seriously consider the cost and risk associated with their greenhouse gas emissions.

What’s the timeline?

Transition - 1 October 2023 to 31 December 2025: This period is designed to allow importing companies and their suppliers to familiarise themselves with the calculation and reporting process, as well as to give EU officials an opportunity to see how the mechanism interacts with other carbon pricing systems worldwide. Affected businesses should use this time to assess the medium and long-term reporting process and cost implications.

Information required:

- Total quantity of goods imported in the preceding quarter (in MWh for electricity and in tonnes for other goods) for each installation producing the goods;

- The total embedded and indirect emissions for goods from each installation (in tonnes of CO2e MWh for electricity and in tonnes for other goods);

- The carbon price, if any, in the country of origin for the embedded emissions.

This will be required on a quarterly basis from importers via customs declarants or indirect representatives, on goods imported during that quarter of the calendar year, detailing direct and indirect emissions.

From 31 December 2024, importers must have ‘authorised CBAM declarant’ status to qualify for the import of in-scope goods. The penalties for non-compliance will be Euro10-50/t of unreported emissions, dependent on the length and gravity of the failure to report. If no action is taken to correct the non-compliant reports, the importer then risks losing their ability to import.

Definitive period - 1 January 2026 to 2034: From the start of the Definitive period, importers will need to purchase and surrender CBAM certificates corresponding to the price that would have been paid had the goods been produced within the EU ETS. CBAM certificates will be priced at the weekly averages of EU ETS allowance auctions. During the calendar year, the importer must ensure that the number of certificates in its CBAM registry account at the end of each quarter corresponds to at least 80% of the embedded emissions in imported products since the beginning of the calendar year. The final annual true-up will mean the importer must surrender CBAM certificates equal to the emissions embedded in goods imported in the calendar year, in addition to submitting an annual CBAM declaration. The emissions covered by the certificates will need to be checked by a verifier.

In 2026, the CBAM will only apply to 2.5% of the emissions created, which is in direct proportion to the reduction of free allowances allocated to EU producers under the EU ETS. The CBAM coverage will continue to increase, and free allocations decrease to EU emitters, until it reaches 100% in 2034 and free allowances are completely phased out. The phase in of CBAM whilst phasing out free allowances to EU producers ensures a level playing field for all.

Penalties during the Definitive period will be more severe than in the Transition period. The penalties for non-compliance will mirror the penalties issued in the EU ETS, which stand at Euro100/t, with the importer in jeopardy of losing their ability to import if they do not pay the penalty.

Summary

Redshaw Advisors provides comprehensive CBAM and Emission Trading System training, tailored to fit sector specific needs. It is committed to providing assistance with reporting requirements, GHG calculations, and EU ETS consultancy for companies exposed both directly and indirectly to the CBAM, including those in the global cement sector.