A detailed delve into the cement market in the Kingdom of Saudi Arabia, historical trends, future prospects, industry consolidation, and the challenges and opportunities ahead.

The Kingdom of Saudi Arabia is a significant player in the global economic landscape, driven largely by oil exports from the second-largest proven oil reserves of any nation. However, recognising the volatility and finite nature of this resource, the country has been actively diversifying its economy. The Vision 2030 initiative, spearheaded by Crown Prince Mohammed bin Salman, aims to reduce the country’s dependence on oil by developing other sectors. A pivotal aspect of this diversification is the cement industry, which plays a crucial role in the nation’s construction and development.

Historical cement trends

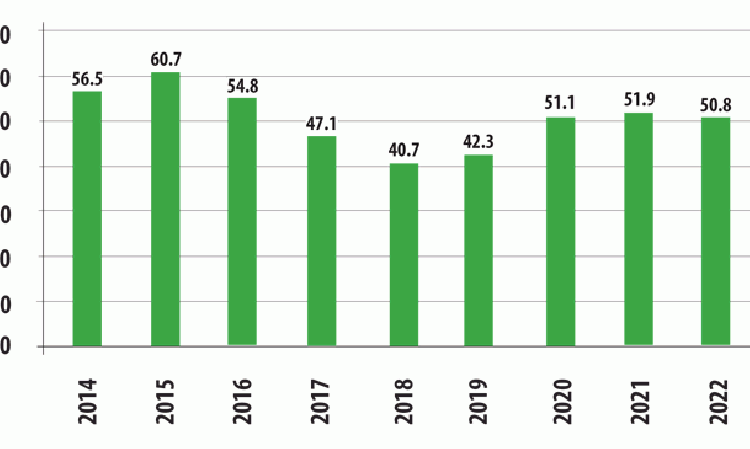

The country has witnessed a cyclic trend in cement consumption over the past decade (See Figure 1). Despite economic contractions, such as the one experienced in 2020, the cement industry showed resilience, growing even during Covid-19 lockdowns. It has witnessed growth of around 3% over the past five years. This phenomenon was largely attributed to construction activities continuing throughout the pandemic. In 2021 and 2022 however, cement consumption experienced a dip. This was due to travel restrictions being removed, which led to expatriate labourers returning to their home countries for a short duration.

Cement in 2022 and 2023

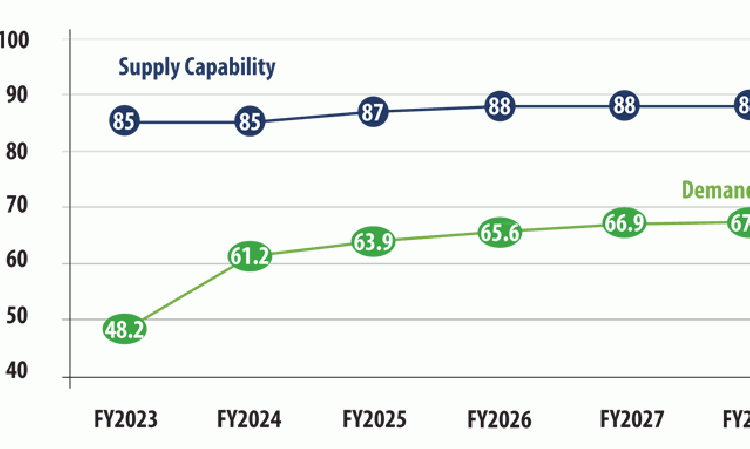

Saudi Arabia had an installed cement capacity of 85Mt/yr in 2023 with 17 players that operate 22 active cement plants. In 2022, the most recent year for which full information is available, total production was 52.6Mt/yr, indicating a capacity utilisation rate of just over 60%. As Saudi Arabia is entirely self-sufficient in terms of clinker production, it does not import clinker or cement. It exports 4 - 5Mt/yr of clinker, mainly to countries in Africa and Asia. Saudi Arabia levies an import duty of 5% on cement, which makes imported cement relatively non-competitive compared to local cement. Saudi Arabia exports 2.0 - 2.5Mt/yr of cement to countries in Africa and Asia.

Per-capita cement consumption in Saudi Arabia is estimated to be about 1470kg/yr. While high by global standards, this is not exceptional within the Middle East. The UAE’s per-capita consumption is 1185kg/t, Oman’s is 1825kg/yr, Kuwait’s is 1325kg/yr, Bahrain’s is 1010kg/yr and Qatar’s is 1790kg/yr.

Main players’ capacities and sales

Industry consolidation is commonly measured using the Herfindahl Index (HI), where 0 indicates perfect competition and 1 indicates monopoly. The HI in the cement industry in Saudi Arabia <0.10, indicating a diverse and competitive landscape.

The top three players in terms of capacity are Saudi Cement, Southern Province Cement and Yanbu Cement, which hold about 37% of capacity combined. The remaining 63% is held by 14 players with capacity shares of 2 - 7%. Most plants are integrated, with just two players that operate grinding units. These are Eastern Province Cement Company at Dammam (1.0Mt/yr) and Najran Cement Company at Najran (2.0Mt/yr).

Yamama is the leader in Saudi Arabia in terms of cement sales, with a 13% market share. It is followed by Southern Province Cement on 11%. Other major players include Saudi Cement, Qassim Cement and Yanbu Cement with 10%, 8% and 8% market shares, respectively. Riyadh Cement and Arabian Cement have market shares of 7% and 6%, while others have shares of 3-5%.

Resources

The cement industry in Saudi Arabia has a wealth of resources at its fingertips. There is adequate limestone to support its current and planned clinker capacities. Gypsum is sourced locally and its supply is not a constraint. Plant technology is seen to be contemporary, with key performance indicators (KPIs) that meet global standards.

The most commonly use fuel is heavy fuel oil (HFO), of which plants have fixed quotas. HFO is provided at a subsidised rate by the government via the national oil company Aramco. However, it is likely that subsidies will be removed in the near future, at which point a shift towards gas is expected.

A regional look

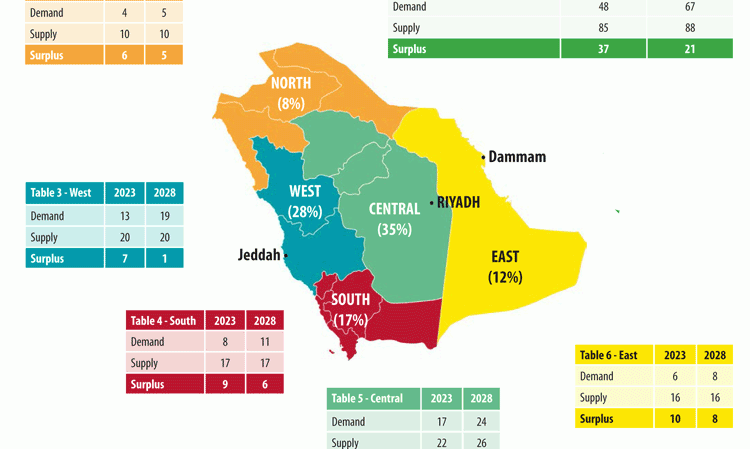

Saudi Arabia divides its cement market into five sub-regions: North, Central, East, West and South. Cement demand and capacity is highest in the Central region, whereas the North region has the lowest cement demand and capacity. All regions have cement surpluses and are estimated to retain these in the near future. By 2028, however, it is estimated that the gap between capacity and demand will reduce to around 21Mt/yr. Nevertheless, it does not necessarily mean that plants located in regions with higher surpluses will have lower capacity utilisation, as there are inter-regional cement sales. Cement demand-supply balance at regional level is depicted in Figure 3.

Cement consumption in Saudi Arabia is concentrated in urban areas like Riyadh, Jeddah and Dammam, with the central region accounting for around 35% of the country’s cement consumption. The demand dispersion is largely influenced by the degree of urbanisation and population density.

Types of cement

The cement market predominantly consumes ordinary Portland cement (OPC), which represents 70% of all sales. Sulphate-resistant cement (SRC) and Portland pozzolana cement (PPC) represent 20% and 10% of the market, respectively.

SRC is more popular in coastal areas or where the foundations are deep and the soil presents the risk of sulphate attack. The use of PPC is limited to the West Region, due to the locations of natural pozzolana deposits.

Modes of sale

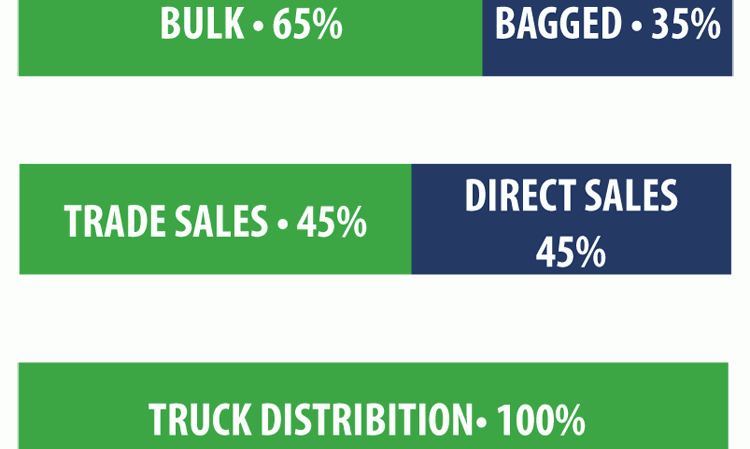

Around 65% of the cement consumed in Saudi Arabia consists of bulk cement and the remaining 35% is bagged cement. Traditionally, cement players have sold cement ex-works, where customers - through distributors - arrange for transportation of the cement from the plant to their site. Only large customers like big ready-mix concrete players with their own cement transport facilities will buy cement directly on an ex-works basis.

About 55% of cement is sold through trade channels. This means that it is distributed from the cement plant through a network of dealers and retailers, who sell it on to end users. The other 45% is dispatched by the cement companies directly to the end user. Cement transport within the country is believed to be 100% by road.

Housing is the major end user segment with 50% cement being consumed by this segment, followed by infrastructure, which consumes around 30% cement. The remaining 20% goes to commercial and institutional buyers to build office spaces, shops, school buildings, hospitals and so on.

Prices

Cement prices in Saudi Arabia are mostly quoted on ex-factory basis with 15% VAT added. Transportation cost and distributors/ channel margin are added to this to arrive at the delivered price. In the fourth quarter of 2023 the delivered price of bulk OPC was US$40 - 50/t in different regions of Saudi Arabia. SRC prices are typically US$3.90-5.30/t higher than OPC. PPC prices are around US$2.70/t lower than OPC prices.

Visions of the Future

The Vision 2030 initiative is a pivotal force driving the diversification of Saudi Arabia’s economy. Cement demand is intricately tied to infrastructure and housing development, with Giga Projects like NEOM - a futuristic linear city, and the Red Sea Project transforming the nation’s landscape. These endeavours, coupled with governmental other initiatives and rising private investment in housing, are expected to drive cement demand in the coming years.

Saudi Arabia also faces a more conventional housing shortage, especially in urban areas. Plans are underway to build over 555,000 new homes across the Kingdom, including major projects like NEOM. The country’s rapid population growth and urbanisation further underscore the need for increased infrastructure development. Saudi Arabia’s economy grew at around 4% and 9% (real GDP growth) in 2021 and 2022, respectively, after contracting in 2020. As per World Bank estimates, Saudi Arabia’s GDP is estimated to grow at an average of 3%/yr over next 4-5 years.

Aside from the economy, cement demand is influenced by population and construction growth, levels of urbanisation, fixed gross capital formation and more. An estimate based on a quantitative analysis of these factors coupled with other determining aspects like socio-political environment of the country, upcoming construction and infrastructure projects and market sentiment point towards a cement demand CAGR of 7% in the next 4 - 5 years.

The industry is thus poised for expansion, with around 3Mt/yr of capacity to be added over the next five years. This will mean that the total installed capacity will reach 88Mt/yr by 2028. This anticipated growth, if materialised, is likely to lead to a continued surplus in cement capacity, even with rapid growth in demand.

Concluding remarks

Cement demand in Saudi Arabia has been cyclical in the past. Previously, when the government announced mega projects, the country witnessed double digit growth in cement consumption, followed by a more or less stagnant situation.

However, with Vision 2030 initiatives being implemented and several giga projects underway and many more being planned in the near future, the outlook for the Saudi Arabian cement market is upbeat. There’s now a focus on diversifying into areas like tourism, entertainment and technology. The goal is to create a more dynamic and sustainable economy. To attract foreign investment, Saudi Arabia has opened up its stock market to international investors and introduced various economic reforms.

While challenges exist, the potential for growth and diversification in the cement sector remains strong. As the nation continues on its path of economic transformation, the cement sector is set to play a pivotal role in shaping Saudi Arabia’s future.