How low-carbon cement projects can be delivered using Carbon Contracts for Difference (CCfDs).

Carbon capture, utilisation and storage (CCUS) projects are capital intensive and involve substantial investment in CO2 capture technology, transport and underground storage. These technologies can decarbonise the cement sector but require patient, long-term investments, often running into the billions of Dollars or Euros. The risk of fluctuating CO2 prices, along with uncertainties around the efficacy of capture technology and regulatory frameworks that will govern transport and storage deter private investors. In the absence of tools to mitigate these risks, the development of CCUS infrastructure will struggle to gain momentum.

Government policies play a significant role in addressing these financing challenges. Tax credits, carbon pricing and public-private partnerships can provide some of the necessary funding, but they often lack the stability and predictability needed to secure private investment. This is where Carbon Contracts for Difference (CCfDs) come into play.

The EU ETS: What’s under the hood?

As governments struggle to balance their budgets and most of the world’s investable capital rests in private hands, large-scale CCUS projects must find ways to tap global capital markets. ‘Cap-and-trade’ initiatives are the foundation of emissions trading schemes (ETS). Such initiatives enable robust, legally-enforceable instruments like CCfDs to thrive

So, how does an ETS work and how can it set a reference price for CCfDs? Established in 2005, the European Union Emission Trading Scheme (EU ETS) is the first international trading system for CO₂ emissions. EU Allowances (EUAs) are statutory allowances that permit companies covered by the EU ETS to make a market in emissions. One EUA entitles the holder to emit one metric tonne of CO₂. EUAs can be bought and sold on the ETS market, and the variable market price of EUAs reflects the avoided cost of reducing emissions.

EU Member States’ National Allocation Plans (NAPs) determine the total quantity of EUAs each may grant to their companies. EUAs may then be sold or bought by the companies themselves. Each Member State must decide, based on forecasts, how many EUAs to allocate to domestic emitters during a trading period and how many EUAs each plant covered by the EU ETS will receive.

This process establishes an EU-wide cap in a decentralised, bottom-up way in which the sum of the NAPs is the overall cap. The first trading period ran from 2005 to 2007, the second from 2008 to 2012 and the third from 2013 to 2020. We’re now in the fourth period which runs from 2021 to 2030. Thus, Member States limit CO₂ emissions from the energy and industrial sectors by allocating allowances, thereby creating scarcity, thus enabling a functioning market to develop.

CCfDs: A financial shield for CCUS

A Carbon Contract for Difference (CCfD) is a financial instrument that guarantees a stable price for carbon credits or emissions reductions over the term of the contract. It provides a hedge against the volatility of carbon prices. If the market price for carbon falls below a specified ‘strike price,’ a CCfD agreement provides that the government or agency counterparty compensates the project developer for the difference. Conversely, if the market price exceeds the strike price, the developer pays the excess to the guarantor.

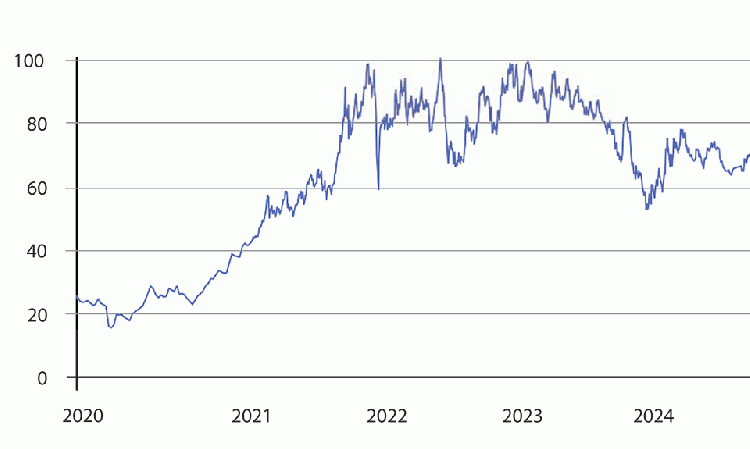

Thus, a CCfD entitles the beneficiary to a payment equal to the difference between a fixed ‘strike’ price, set by contract, and a variable reference price such as the exchange-traded EU ETS market price. Pledging this instrument as collateral can rapidly scale project finance when the emitter’s levelised cost-per-tonne of CO2eq avoided falls below its quoted market price under the EU ETS and similar schemes. EU ETS prices traded around €70 - 80/t in the past six months, though they exceeded €100/t in the second quarter of 2022.

CCfDs create a reliable revenue stream for CCUS projects by insulating them from market volatility. This risk mitigation allows developers to secure financing, as the contractually-guaranteed carbon revenues can be used as collateral for loans. In regions with fluctuating carbon prices or nascent carbon markets like Indonesia, CCfDs are essential for developers to achieve a final investment desision (FID) for CCUS projects.

Real-world initiatives

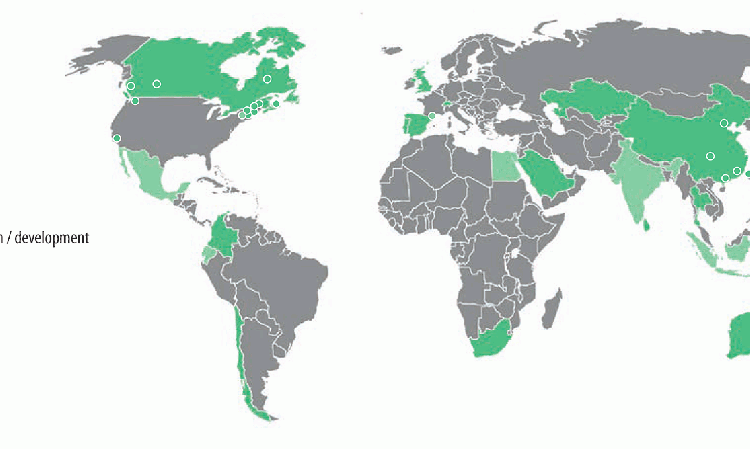

Based on the success of the EU ETS, carbon market trading schemes now operate in Australia, New Zealand, South Korea, China and California (US), as well as the UK, where the scheme split from the EU ETS post-Brexit. They are becoming more widespread, particularly in Asia, for example in Indonesia, which recently announced plans for a mandatory ETS. Several high-profile examples demonstrate how CCfDs enhance the bankability of CCUS projects by reducing financial risk and fostering private sector participation.

Canada’s Groundbreaking Carbon Credit Offtake Agreement: Canada is a pioneer in implementing CCfD-like instruments to achieve final investment decisions for CCUS projects. The Canada Growth Fund (CGF), a public investment vehicle, signed the country’s first CCfD-style agreement, known as a Carbon Credit Offtake (CCO), with Calgary-based carbon capture firm Entropy Inc.

Entropy and CGF entered into a CCO agreement whereby CGF will purchase from Entropy’s gas-fired power plants up to 9Mt (0.6Mt/yr over a 15yr term) of TIER (Alberta’s Technology Innovation and Emission Reduction Act) equivalent carbon credits. The CGF also invested US$200m of equity in Entropy, further de-risking the project.

Entropy’s first CCO deal is the Advantage Glacier Phase 2, the second of two post-combustion power-gen projects. This will produce up to 0.192Mt/yr of CO₂ (including 32,000t/yr from Phase 1) for a total of approximately 2.8Mt over the 15-year term. With this CCO agreement in place, at an initial price of US$86.50/t, CGF bears the carbon pricing risk for the project.

The total cost of Glacier Phase 2 capture equipment, compression, transportation and storage wells is US$127m, yielding 0.16Mt/yr of CO₂. That’s about US$800/t/yr rated capacity, of which US$200/t/yr is allocated for compression, transportation and storage. CO₂ will be injected and stored in a saline aquifer 2km below the surface.

Project revenue is contractually underpinned to the tune of 75% by a 15-year Carbon Credit Offtake agreement with CGF and 25% by a 15-year Power Purchase Agreement (PPA) with Advantage. The certainty provided by the CCO enabled Entropy to reach FID in July 2024.

Entropy’s successful financing is a textbook example of how CCfDs help sponsors achieve FID for innovative CCUS projects and capture technologies.

Germany’s Klimaschutzverträge: A model for heavy industry decarbonisation: In 2023, Germany launched a CCfD program called Klimaschutzverträge (Climate Protection Contracts), to help heavy industries, including cement, steel and chemicals, decarbonise their operations. Under this program, the German government pays the difference between the carbon strike price (the cost of carbon abatement technologies) and the price of carbon on the EU ETS market for contract periods of up to 15 years. This provides long-term price certainty to companies that invest in decarbonisation technologies, even in a volatile market.

The program, essential to Germany’s decarbonisation strategy, specifically targets hard-to-abate sectors like cement and steel which have been reluctant to invest in costly technologies. By providing a financial safety net, the government effectively mitigates the risk of market instability, giving industries the confidence to adopt CCUS and other mitigation technologies. The EU is also moving toward promoting CCfD-like structures through initiatives such as the Innovation Fund.

Others: Beyond Germany and Canada, other regions are increasingly looking to CCfDs as a tool to accelerate CCUS deployment. The UK is exploring similar models through its CCUS Innovation Programme and other initiatives. The success of these programmes and attendant learnings in Europe and North America provide a roadmap for broader global adoption, particularly in emerging markets where financing for CCUS projects remains scarce.

CCfDs compared to other mechanisms

While CCfDs provide a compelling solution for de-risking CCUS projects, they’re not the only mechanism available to support such projects. Tax incentives, carbon pricing and blended finance also play important roles.

1. Tax credits: Programs like the US 45Q tax credit provide a direct financial incentive for carbon capture, granting US$85/t of CO₂ captured and stored. While tax credits can reduce upfront costs, their value is capped by the tax liability of the project developer – unless they can find a tax equity partner to assume that liability. Furthermore, the 45Q program has a 12-year expiry and is necessarily subject to political changes, which adds uncertainty for investors.

2. Carbon pricing & ETS: Carbon taxes and cap-and-trade ETS are essential in driving demand for CCUS technologies. However, the unpredictability of carbon pricing, particularly in regions with less-established markets, can create challenges for securing investment in CCUS infrastructure. Unlike CCfDs, carbon pricing mechanisms offer no market-based guarantee of stable, predictable revenue.

3. Blended financing, direct subsidies and grants: Blended financing, where public funds are used to leverage private investment, can also support CCUS projects. This approach generally involves government-backed loans or equity co-investments. This is the case for Norway’s Northern Lights project in Brevik and the Netherlands’ €2.1bn Porthos CO₂ collection hub in Rotterdam. While effective in some contexts, blended financing still relies on market conditions and fickle public policy, which may change over time.

When compared to these other mechanisms, only CCfDs provide the long-term stability needed for large-scale CCUS deployment. The fixed-price nature of CCfDs makes them a more reliable tool for attracting private capital, especially in markets with uncertain or fluctuating carbon prices.

Conclusion

The financing challenges of CCUS projects are significant, but CCfDs provide a viable solution to de-risk investments and enable large-scale adoption of carbon capture technologies. Real-world initiatives, particularly in Canada and Germany, demonstrate how CCfDs can support the bankability of CCUS projects, providing financial certainty that encourages private sector participation.

As policy makers continue to develop supportive frameworks and as carbon markets mature, CCfDs will play an increasingly important role in the global effort to decarbonise hard-to-abate industries like cement and steel. For investors, understanding the financial mechanics of CCfDs – and their ability to transform the risk profile of CCUS projects – is key to unlocking the billions in capital needed to finance a low-carbon future for the global cement sector.