To tie in with the location of the 59th IEEE-IAS/PCA Cement Industry Technical Conference, Global Cement turns its attention to the cement sector of Canada, with a look at production trends, producers and the future.

Cement production trends

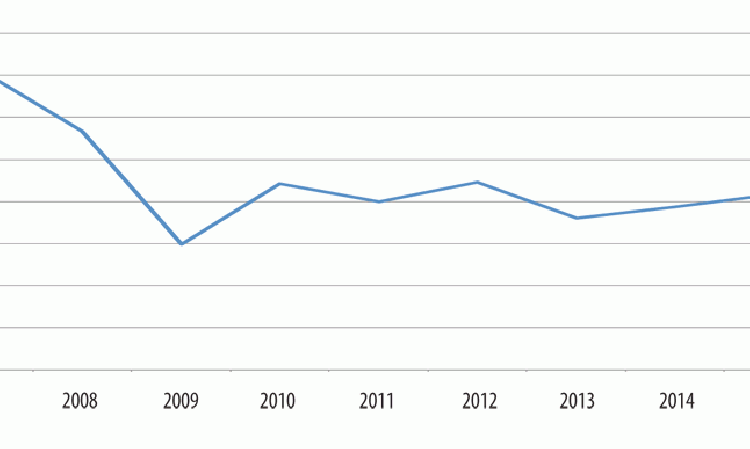

Cement production in Canada rose from 12.6Mt in 2000 to 15.1Mt in 2007. However, with the onset of the global economic downturn, production fell by 9.3% to 13.7Mt in 2008 and by a further 19.7% to 11.0Mt in 2009. As Figure 1 shows, production has since levelled out at around 12Mt/yr, with slight fluctuations year-on-year. In 2016 the country made 11.9Mt of cement, a 2.4% fall from 12.2Mt in 2015.

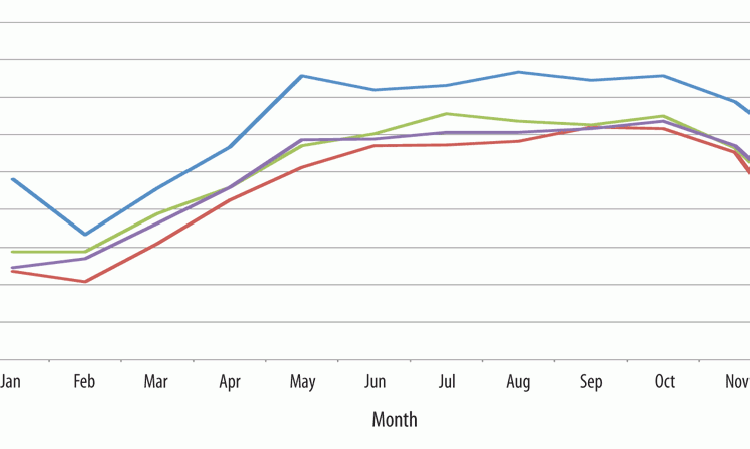

Figure 2 shows monthly Canadian cement production totals for selected years between 2007 and 2016. This shows the wide gulf between the recent peak in production in 2007 and the slump in 2009, as well as data for 2016 and a hypothetical ‘median year’ derived from median monthly production figures for the 2007 - 2016 period. This shows that Canadian cement production in 2016 was very close to recent norms. Over 12 months it was slightly behind the median year, which clocked 12.2Mt of cement ‘made.’ Secondly, Figure 2 demonstrates the monthly range of cement production, which is highly seasonal due to the country’s wide range of weather.

Cement export trends

Canada is a net exporter of cement, most of which has historically been sent to the US. However, the slump in US demand for cement reduced the amount exported from over 5Mt in 2004 to under 3.0Mt in 2010. Over the next five years, exports stabilised at just over 3Mt/yr, rising to 3.6Mt in 2016.

Cement in the Provinces

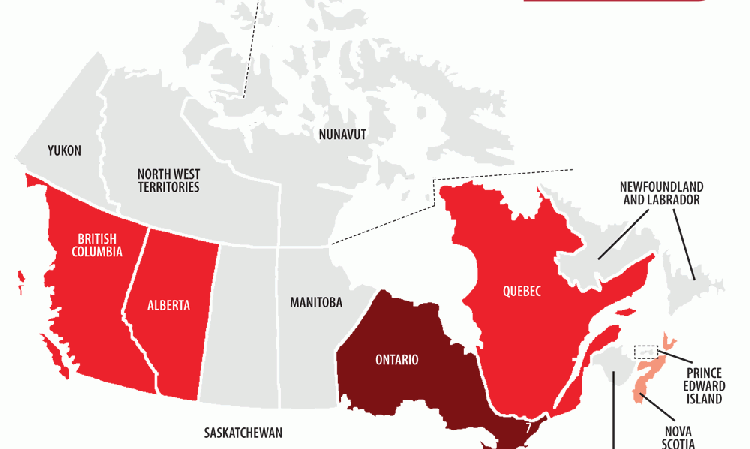

Ontario, Canada’s most populous Province, with 38% of the population, is also by far the largest regional consumer of cement in Canada. In 2016 it saw cement shipments of 3.2Mt, around 38% of the 8.3Mt of cement despatched to the whole of Canada. The second most cement-hungry Province was Quebec, which had shipments of 2.0Mt, around 24% of the national total. It has 24% of the country’s population.

While Statistics Canada collects data for cement shipments in each Province and Territory, it cannot publish it all as this would expose the shipments of individual plants in regions where there are only one or two producers. It is only possible to say that the remaining 11 Provinces and Territories saw shipments of 3.1Mt of cement between them, around 38% of national despatches. They also share 38% of Canada’s inhabitants.

Cement producers

Canada’s cement industry comprises 15 currently-active integrated cement plants, one ongoing project and one plant proposal. (See Figure 3). The active plants share 16.4Mt/yr of capacity, giving a national capacity utilisation figure of around 73% in 2016. There are no grinding-only cement plants in Canada.

Multinational players account for 15.6Mt/yr, or 95% of Canadian cement capacity. In descending order of capacity they are: LafargeHolcim (6.0Mt/yr), HeidelbergCement (4.5Mt/yr), CRH (3.1Mt/yr) and Votorantim (2.0Mt/yr).

LafargeHolcim: The world’s largest multinational operates five cement plants under its Lafarge Canada subsidiary and is spread across all of Canada’s five cement making Provinces. The assets are legacy Lafarge units from before the establishment of LafargeHolcim in 2015. Legacy Holcim plants in Canada were acquired by CRH as part of its extensive acquisition of Lafarge and Holcim’s divested assets.

HeidelbergCement: The second-largest producer of cement in Canada, Germany’s Heidelberg-Cement is active via its long-standing subsidiary Lehigh Hanson, which operates plants in Alberta and British Columbia.

In 2016 it also acquired Italcementi’s Essroc Canada and Ciment Québec subsidiaries, which operate in Ontario and Quebec, as part of its wholesale takeover of the Italian multinational. This has given HeidelbergCement a more even spread between the east and the west of Canada.

CRH: Active in Canada since 2015, Ireland’s CRH bought the former Holcim subsidiary Essroc as part of its major acquisition of Lafarge and Holcim divestments. It operates two plants with a shared capacity of 3.1Mt/yr.

Votorantim: Votorantim acquired Canada-based St Marys Cement, which was established in 1912, in 2001. It continues to operate the ‘original’ St Marys plant (0.8Mt/yr) and the newer Bowmanville plant (1.3Mt/yr), both of which are located in Ontario. The company also operates four cement plants in the US.

McInnis Cement: When it begins production later in 2017, McInnis Cement will become a major player in the Canadian and wider North American market. The 2.2Mt/yr plant, first proposed in the 1990s, is owned by a number of independent investors and is scheduled to come online in the first half of 2017. thyssenkrupp Industrial Solutions (USA) is the main contractor. McInnis’ arrival on the Canadian cement scene will increase national capacity to 18.9Mt/yr, although its location on the St Lawrence Seaway is intended to facilitate significant exports to the US.

Even before it has begun production, McInnis Cement has not had the most straightforward entry to the market. Given that the plant intends to target the US market, McInnis has faced legal action from US producers and, when it appeared to bypass usual environmental clearance procedures in 2013, Lafarge Canada joined forces with environmental NGOs to complain. McInnis has made great efforts to reassure all stakeholders that its construction and operation will conform to all environmental regulations, which, in Canada, are among the most stringent in the world. It has also sought to reassure Canadian producers that it will not adversely affect the supply situation in the north east.

The project has also been under intense public scrutiny due to the fact that the Quebec government has ploughed some US$350m into the project in return for a minority stake (this was a major reason behind the US industry’s objection). The Province’s public pension fund manager has also invested US$100m. Then, in June 2016 the CEO was forced to step down after the project over-ran its budget by US$350m.

The news more recently out of McInnis Cement has been more positive. It has appointed a new CEO, quelled investor concerns, made significant progress with its Sainte-Catherine terminal and announced a 140,000t cement transit agreement with the Gaspé railway corporation.

Federal White Cement: A small independent manufacturer of cement, Federal White Cement has been in operation since 1979. Updates in 1999 and 2007 have brought its capacity up to 0.5Mt/yr.

Colacem Canada: Colacem Canada, a unit of the small Italian player Colacem, is the smallest producer of cement in Canada. Its plant at Grenville-sur-la-Rouge has a capacity of just 0.3Mt/yr.

Colacem Canada recently proposed plans for a new 3000t/day (1.2Mt/yr) integrated cement plant near to a limestone quarry that it operates in L’Original, Ontario. However, one of two local councils voted against the plans in January 2017, blocking them. It is unclear if the company will resubmit the plans.

Future scenarios

Due to low oil prices, Canada’s otherwise sturdy economy has taken a knock in recent years. However, In January 2017 the International Monetary Fund (IMF) maintained its 1.9% GDP growth forecast for Canada for 2017, a rise from an estimated 1.3% in 2016. The IMF forecasts Canada’s GDP to grow by 2.0% in 2018, indicating strong prospects for the cement sector going forward. Both forecasts are identical to the IMF’s growth forecast for its Advanced Economies group. For comparison, the IMF increased its forecast for the US to 2.3% for 2017 and 2.5% for 2018.

Despite the apparent strong fundamental growth in the economy, the prospects for the Canadian cement sector will continue to depend on oil price recovery and how relations with the new US Administration develop. Demand for cement in the US will play a factor into how much cement McInnis will be able to export, directly affecting the amounts available inside Canada. If the US consumes less than expected, Quebec, and Canada, could find itself swamped with extra cement capacity.