Contraction of the Chinese cement sector has accelerated due to the Covid-19 outbreak...

China is the most highly-populated country in the world, with an incredible 1.43bn estimated inhabitants in 2019. This total, nearly a fifth of the world’s entire population, is unevenly spread across a country that represents only 6.4% of the earth’s total land, despite being the fourth-largest country in the world. Within China, the vast bulk of inhabitants are concentrated in the south and west of the country. This has led to the development of numerous mega-cities unlike any seen in the rest of the world. Such developments, as well as many thousands of major infrastructure projects, have been served well by an enormous and centrally-planned domestic cement sector.

China’s low labour costs and centrally-planned economy enabled it to become the ‘world’s factory’ during the latter part of the 20th Century. In 2018 China was home to 20% of global manufacturing output.However, China’s emerging middle class, associated rising wage demands and hightened environmental concerns have steadily eaten into China’s historical manufacturing advantage. In the future this will be further hampered by China’s former one-child policy (1979 - 2015), which has ensured a rapidly-aging population. China’s median age in 2020 is around 39. By 2050 it will be around 49.5, older than Japan’s present 47.3 years. By this time, China’s overall population will have shrunk by 60 million, albeit to a still rather large 1.37bn.

Cement industry background

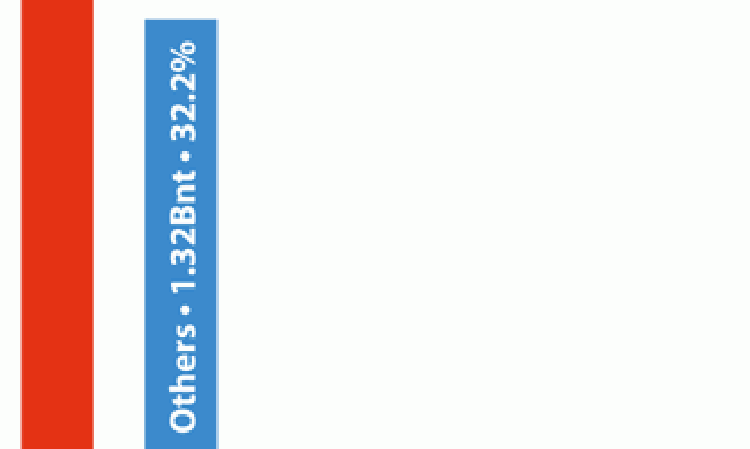

As Figure 1 demonstrates, China is the world’s largest cement sector by a considerable margin. It has produced more cement than the rest of the world combined every year so far during the 21st Century.China’s cement production rose from ‘just’ 500Mt/yr in 1995 to over 1Bnt/yr by 2005. It made more than half of the world’s cement for the first time in 2007 and, by 2014, production had skyrocketed to 2.45Bnt. Cement production in 2019 was approximately 2.2Bnt, unchanged from 2018, which was, in turn 6.1% lower compared to production in 2017. This means that the sector’s output has contracted by around 300Mt, equal to the cement produced by India in a year, since 2014.

The emphasis on contraction in the cement sector is led directly from the top of the Chinese government, as the country has now clearly passed the largest excesses of its mid-to-late 2000s building boom. The cement sector grew in an excessive fashion to meet the demand for new buildings and entire cities, some of which remain unoccupied to this day.

In 2013, China’s State Council issued its ‘Guideline to tackle serious production overcapacity,’ including in the cement sector. At the same time, the Chinese Cement Association (CCA) drafted plans to promote mergers and acquisitions in the sector. In 2017 the CCA stated that 393Mt/yr of clinker capacity and 540 small to medium-sized cement grinding plants would be closed by 2020. A complete ban on new capacity was announced by the Ministry of Industry and Information Technology (MIIT) in February 2018. There has also been consolidation, most notably the merger of CNBM and Sinoma to produce the world’s largest cement producer, with more than 500Mt/yr of capacity, in 2018. The aim of all of these measures is to reach clinker and cement capacity utilisation rates of 80% and 70% respectively.

Speaking on Global Cement Live on 23 April 2020 Ian Riley, the President of the World Cement Association (WCA) and long-standing participant in the Chinese cement sector, stated that, while the average cement capacity utilisation rate was 71% in 2019, this headline conceals a disparity. While the cement industry in the north of China operated at a capacity utilisation rate of 48% in 2019, the south was already up at 80%. This is due to the fact that construction projects and cement production in the north have historically been halted for four months over the winter. Due to the government’s capacity reduction policies, this approach became nationwide in 2016, with enforced closures of 80-100 days/yr in all provinces since 2017. With further capacity cuts to come, the cement capacity utilisation rate of 70% is already a tough target.

Turning green

Capacity restrictions have gone hand-in-hand with tighter emissions standards for cement production. Firstly, premiums were charged for power consumption above a given rate, in order to drive production efficiency. Since 2016 plants that fail to meet the most recent (2013) standards of 30mg/Nm3 for dust, 200mg/Nm3 for NOx and 400mg/Nm3 for SO2 have faced closure or been ordered to clean up their act.

In 2018 Henan Province introduced ultra-low standards (10mg/Nm3 for dust, 50mg/Nm3 for NOx and 100mg/Nm3 for SO2). It was followed in 2019 by Hebei Province (10mg/Nm3 for dust, 30mg/Nm3 for NOx and 100mg/Nm3 for SO2). This has led to a raft of upgrades by plants that didn’t want to go out of production. In the longer term it is likely that emissions reductions will drive demand for alternative fuels and a move away from China’s traditional use of coal for cement production.

Profitability rollercoaster

Since the onset of supply-side reductions by the Chinese government, the country’s cement producers have been on a profitability rollercoaster. Production peaked at 2.4Bnt in 2014 but profits were hit hard in 2015 as production capacity was not met by demand. Producers were able to recover some of their lost profitability in 2016 as supply reductions led to higher prices. 2017 was a stronger year again, based in part on expansion efforts overseas. Price rises continued into 2018, enabling further stabilisation of balance sheets.

Data from the Ministry of Industry and Information Technology (MIIT) showed that China’s cement sector’s net profit grew by 20% year-on-year to US$26.6bn in 2019 from US$22.3bn in 2018. The sector’s total revenues reached US$144bn, representing an increase of 13% from US$128bn. It appeared that the sector’s profitability has been secured, even if it was still making vast quantities of cement.

CNBM-Sinoma recorded a net profit of US$2.48bn in 2019, a 27% year-on-year increase compared to US$1.95bn in 2018. Its revenues rose to US$36.0bn in 2019 from US$30.7bn in 2018, a 17.3% year-on-year rise. Meanwhile, Anhui Conch Cement recorded a net profit of US$4.77bn in 2019, 13% higher than its 2018 net profit of US$4.23bn in 2019. Revenues rose by 22% year-on-year to US$22.2bn from US$18.2bn in 2018.

Enter the ‘novel coronavirus’

The strong performance seen by many Chinese cement producers in 2019 will now most likely be looked back upon as the start of a new profitability rollercoaster. This is due to the coronavirus outbreak, which first rose to prominence in Wuhan, Hebei Province in the autumn of 2019. The region was the first of many to see ‘lockdown’ conditions, which soon spread across China and the rest of the world.

Construction, and hence cement production, was adversely affected. Across China, cement production fell by 29% year-on-year to 150Mt in January and February 2020 combined, already the quietest months of the year due to Chinese New Year. Output then picked up to 149Mt in March 2020, 17% lower than in March 2019. On the demand side, reporting from the Chinese Cement Association reveals that national infrastructure investment (excluding electricity) decreased by 19.7% year-on-year in the first quarter of 2020. National real estate development investment for the quarter fell by 7.7% to US$310bn.

While construction projects were allowed to resume in Hebei Province as early as the end of March 2020, in areas away from Wuhan, progress was initially limited due to workers being locked down away from worksites after the New Year holiday. Three weeks after measures were relaxed, the average shipping rate for cement producers was only 60% of the regular rate in these areas. In Wuhan itself the situation was more stark, with demand for cement at only 20% of expected levels at the time the lockdown ended on 8 April 2020. Data from the Hubei Cement Association shows that only half of Hubei province’s 57 clinker production lines were producing cement on 30 March 2020, with the rest suspended.

Across China, producers felt the full brunt of the coronavirus outbreak in their first quarter results. Anhui Conch’s first quarter profit was US$690m, down by 19% year-on-year from US$860m in the corresponding period of 2019. Sales fell by 24%, to US$3.28bn from US$4.31bn. Huaxin Cement announced a predicted profit drop of 46% year-on-year in the first quarter of 2020, to US$100m from US$188m in the corresponding three months of 2019. Its sales were down by more than a third. Meanwhile, Shanshui Cement has said that it expects its first-quarter losses to rise year-on-year in 2020.

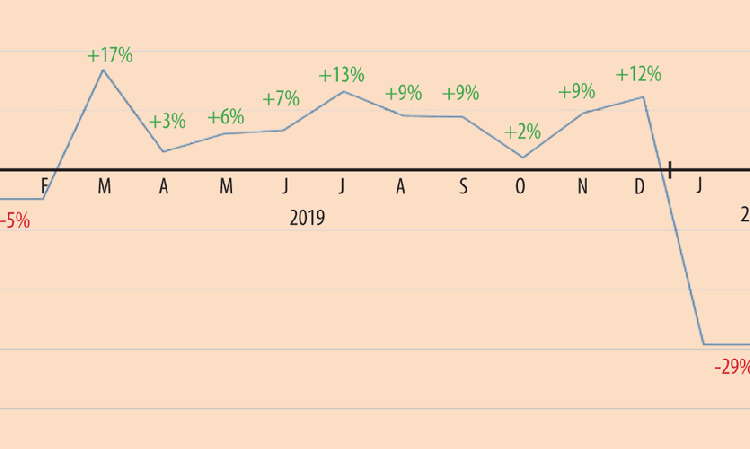

However, the Chinese cement sector appears to have bounced back strongly in the second quarter of 2020. Although second-quarter results were unavailable at the time of going to press, the Ministry of Industry and Information Technology published data showing 94% domestic cement production capacity utilisation in the two-week period ending 10 April 2020. This, it reported, followed the end of coronavirus-related plant shutdowns in all provinces. Figure 2 shows that April 2020 sales exceeded those of April 2019. For the first four months, sales were 14% lower than in 2019. The May 2020 values will make interesting reading.

A note on prices

All-China 42.5 grade cement spot prices from sunsirs.com were US$66.48/t on 22 May 2020, around 13% lower than at the start of January 2020. Some price reduction is usual around Chinese New Year (25 January 2020), but the magnitude and length of the decrease have both been extended due to coronavirus-related closures.

Prices in late May 2020 were very similar to those of early April 2020 in both US Dollar and Chinese RMB terms, but had dipped to around US$65.55/t between 10-26 April 2020. Forecasters had earlier expected that prices would start to recover during the second half of 2020 on the back of higher demand, particularly from the recommencement of infrastructure projects. However, the main thrust of any price rise now seems to have been delayed to the third quarter at the earliest.

Looking ahead

In Covid-19 Impact Analysis CIC 2025, its extensive new report on the effects of the coronavirus outbreak on global cement production, OneStone Consulting forecasts that China’s cement capacity utilisation will fall to 70% in 2020 from an estimated 74% in 2019. This will translate into a 8.5% decline in cement production in 2020 compared to 2019 to around 2.1Bnt. For 2021 it expects further contraction of 3.3% to around 2.03Bnt. This will be due to continuation of China’s supply side changes. Before the coronavirus, OneStone already expected production to fall by about 2% in 2021 compared to 2020. It appears that the coronavirus outbreak has inadvertently sped up the process of Chinese cement capacity reduction.

In its report, OneStone Consulting also estimates that the plant closure rate will soon overtake the overall decrease in production, leading to higher utilisation rates. It concludes that, by 2025, China will lose a further 570Mt/yr of cement production capacity and have cut production by around500Mt/yr. This leads to a headline production figure of 1.85Bnt by 2025, around the same as last seen in 2010. Over the same period, OneStone Consulting forecasts that the rest of the world will increase its cement production total to 2.11Bnt, taking more than 50% of production for the first time since the early 2000s. While the expansion around the world will be uneven and chaotic, China’s continued contraction will be a planned and centrally ordered process.

Looking abroad

Given the potential reduction in future sales opportunities at home, it is unsurprising that Chinese cement producers continue to seek new markets. This continues a trend that first took hold at the close of 2017, when it became absolutely clear that China’s domestic capacity would only decrease in the coming years. China’s cement producers and world-leading plant manufacturers became involved in projects across regions associated with China’s Belt and Road initiatives across central and southern Asia, as well as in Africa.

Since the start of 2018, Global Cement has become aware of at least 59 projects across north Africa (6), sub-Saharan Africa (15), the Middle East (3), South America (4) and central (11), north (3), south (8) and south east (9) Asia in which Chinese parties were either the supplier, investor or both. They jointly comprised a total capacity of at least 74.2Mt/yr, with the bulk (52.4Mt/yr) first reported in 2018.

Africa has recently become increasingly important for Chinese-led cement projects in 2019 and 2020. Recent highlights include: the signing of an agreement between Afcham China National Consortium Material Company and Kribi Industrial Cement Plant Company for the construction of a 0.5Mt/yr integrated cement plant in Cameroon; the announcement of a 1.0Mt/yr plant to be built by Sinoma in the Democratic Republic of the Congo, and; the first cement from a Sinoma-built moveable modular grinding mill at a grinding plant in Guinea. Sinoma also commissioned a 3.2Mt/yr plant for PT Cemindo Gemilang in Indonesia in April 2020, ahead of its May 2020 completion date and despite restrictions arising from the coronavirus outbreak.

With options at home limited, Chinese cement players are now also making outright acquisitions rather than new build plants and joint-ventures. West China Cement completed its purchase of a majority stake in Schwenk Namibia for US$104m in January 2020, giving it control of Ohorongo Cement. More recently, Huaxin Cement’s deal to buy ARM Cement’s assets in Tanzania was completed in May 2020. If China’s domestic industry recovers to the point that the major players can continue to invest, we should expect more of the same over the coming months.

Final thoughts

The move away from the ‘worst excesses’ of Chinese cement production since 2014 represents a major achievement for central planners. However, even if China makes 1.8Bnt of cement in 2025, as forecast by OneStone Consulting, and then continues to reduce output at the same rate (75Mt/yr/yr), China will still manufacture 1.4Bnt of cement in 2030. This is sufficient for every man, woman and child that lives there to have 1t (1000kg) every year, vastly in excess of consumption rates in rapidly-developing economies, (~600kg/capita/yr). Adding up the combined totals for the next 10 years shows that, by 2030, China will have consumed another ~17.5Bnt of cement.

This is exceptional in global terms. However, China is also exceptionally well positioned to take action to reduce its overcapacity. It was already on this path due to the increasing importance of environmental regulations. Now, the coronavirus outbreak may take a bite out of cement demand just as the government cuts down on the supply side. While China’s cement industry is not suddenly going to shrink overnight, this opens up at least the possibility of more modest production in future years.