Joe Harder of OneStone Consulting looks at how the cement industry is expanding its cement and clinker capacities, despite the Covid-19 pandemic and overcapacities in many countries, drawing on the findings of OneStone’s new multi-client market report Cement Projects Focus 2025.

The global cement industry is investing in new, modern and efficient cement plants. However, much less new clinker capacity is projected than new cement capacity, the result of the decreasing clinker factor in cement production. The number of dedicated grinding plants is also growing massively. In some cases these grinding plants are receiving clinker from new kiln lines that have no clinker grinding facilities and are therefore different from traditional integrated plants. However, there are many more interesting ‘game changers’, such as the growing number of clay calcination plants and conversions of grey cement lines to make white cement.

Plant contract review

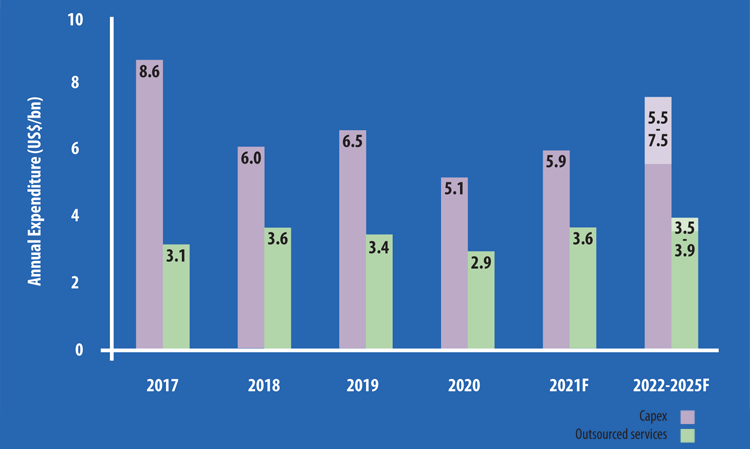

Figure 1 shows cement industry expenditures in the period 2017 to 2021, excluding China. The capital expenditure (capex) investment decreased from US$8.6bn in 2017 to US$5.1bn in 2020, a decline of almost 41%. However, between 2021 and 2025 a massive recovery of up to 47% is projected. A similar picture is seen for outsourced services, including spare parts, plant upgrades and optimisation.

In 2020 Sinoma increased its overseas cement industry order intake to US$2.8bn, from US$1.8bn in 2019. By doing so, it was able to increase its market share from 28% to 55% in a declining market. In 2020 Sinoma contracted 13 new kiln lines and 4 separate grinding plants.

After some years of massive decline, the market in China also recovered. Figure 2 shows how the number of completed new kiln lines developed in China and the Rest of the World (RoW) since 2015. In China the number of completed new kiln lines declined from 31 units in 2015 to ‘only’ 13 in 2017, due to overcapacity issues and restrictions put in place by the Chinese government. However, due to the decommissioning of older plants, approvals for new projects were given and consequently the newly commissioned kiln capacity in China increased from 20.5Mt/yr in 2017 to 38.2Mt/yr in 2020 and then to 48.8Mt/yr in 2021. Meanwhile, the completed new kiln lines in the RoW increased from 34 units in 2015 to 64 in 2018, before falling to 42 in 2020. New completed clinker capacity peaked in 2018, with 88.2Mt/yr, falling to 58.8Mt/yr a year later.

OneStone also analysed the cement plant contracts from 2017 to the first half of 2021 in detail, including greenfield projects, new lines, plant upgrades and separate grinding plants. In total in the period under review it identified 312 projects in the RoW. Of these, 61 were greenfield projects, 92 were new lines, 21 were major upgrades with capacity increases and 138 were separate grinding plants.

Almost 409Mt/yr of new cement capacity and 270Mt/yr of new clinker capacity is provided by these projects. 27.2% of the new cement capacity comes from new separate grinding plants. In the market report, the new contracted capacity figures are provided by year, supplier and region (with 10 world regions). The market shares of the main kiln and cooler suppliers are also provided. In the grate cooler sector, the specialist suppliers IKN, Claudius Peters and FONS recorded a total of 121 new coolers, 60.5% of all new coolers. This is a significantly higher market share than the turnkey suppliers Sinoma, FLSmidth, TKIS and KHD.

Future capacity changes

However, the main focus of the new market report is on the cement capacity expansion projects for completion in the period from 2019 to 2025. Some of these projects have not begun, with no contracts signed at the time of writing (in the fourth quarter of 2021). From the projects already completed or announced, OneStone identified 373 projects, including 80 greenfield projects, 121 new lines, 27 major upgrades and 145 separate grinding plants. Each project has a completion probability of more than 60%, which means that the projects are already in the planning stage, are under construction or already commissioned. Furthermore, we identified another 34 projects, which were cancelled, suspended or delayed and don’t fulfil the before mentioned probability categories. The 373 high probability projects were analysed in detail and are listed project by project in the report annex with parameters such as projected commissioning year, investor, country, location, capacity, type of project and capex figure, if available, as well as the supplier if the project has already been contracted.

Figure 3 shows the breakdown of new cement capacity projections in the RoW of the projects for commissioning by 2025 by type of investment. A peak of the new cement capacity to be commissioned is shown for 2021 with almost 113Mt/yr of new capacity added. This is due to delays to several projects from 2020 as a result of the Covid-19 pandemic and lockdowns at many sites.

Nearly 80Mt/yr of new cement capacity will be commissioned in 2022 and the same amount is forecast again for 2023. These figures could be even higher because the lead time from contracting to plant commissioning of cement plant upgrade and separate grinding plants can be as short as 12 months. Additionally, OneStone found that, of 309 projects completed from 2017 to the first half of 2021, only 11 projects had a lead time of one year, 52% had a lead time of two years, 30% had a lead time of three years and only 7% had a lead time of more than three years. 3% of the projects had lead times in excess of five years.

Are kiln lines getting bigger? Yes and no...

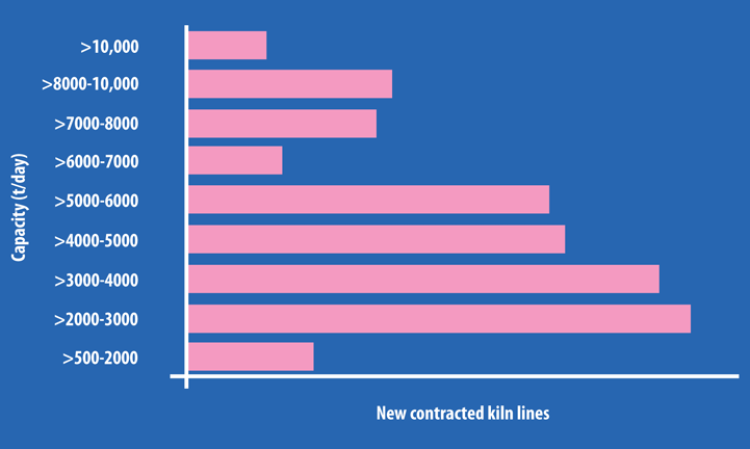

OneStone analysed the kiln capacities of the completed projects and the projects due for commissioning by 2025 in the RoW. Figure 4 shows the new contracted kiln lines from 2017 to 2021. In total there were 153 new kiln lines, excluding kiln upgrades. Kiln capacities up to >6000t/day make up almost 77% of the projects. Kilns with >2000 - 3000t/day have the highest market share with 20.9%. All kiln sizes >8000t/day have a market share of just 11.8%.

However, when it comes to the clinker capacity, kiln sizes up to 6000t/day have a share of 60.2%, while the kilns of >6000 - 8000t/day have a 22.7% share. Large kilns are increasingly being contracted to replace two or three older kilns or to fulfil large capacity projections of ambitious investors in growing markets. Smaller plants are preferred by smaller regional markets and when investors enter new markets, a trend that has not changed much of late.

OneStone also analysed the situation for white cement and clay calcination. White cement projects have seen a recovery after some years of a stagnation. From 2017 to the first half of 2020, nine new projects were contracted. Of these, five are projects where grey cement kilns are being converted to produce white cement. Two more projects have already been announced.

From 2016 to the first half of 2021, there were a total of nine clay calcination projects contracted outside of China, with three more due to complete by early 2022. However, this is a drop in the ocean. If the amount of activated clay in cement is increased from less than 1% in 2020 to about 8% in 2050, as required by the various CO2 roadmaps, then almost 70 new clay calcination lines, each with 1000t/day capacity, will have to be built... every single year.

About the report

Cement Projects Focus 2025 is the 6th edition of this kind of market report by OneStone Consulting. The new report was released at the end of November 2021 and comprises 175 pages with 113 charts and 28 tables. The market report provides a huge amount of data for the cement industry and allows deep insights into the capacity expansion by the cement industry.

The report is recommended for cement companies that have ambitions to set up new projects, as well as plant equipment suppliers that want to understand market shares in the industry and to be informed about new projects. It is also instructive for cement industry analysts and associations.

Email: This email address is being protected from spambots. You need JavaScript enabled to view it.